Situational Awareness: Leopold Aschenbrenner’s AGI Thesis, Hedge Fund, and the Bottleneck Investment Playbook

Research date: 2026-05-08

Data sources: SEC EDGAR 13F filings (via OpenBB SDK), Fortune, Forbes, Yahoo Finance, EA Forum, Substack (Linas Beliūnas, Latticework/MOI Global), Motley Fool, WhaleWisdom, ainvest.com, Syz Group, Lawfare, Medium

13F data: obb.equity.ownership.form_13f('0002045724', limit=5) — SEC EDGAR provider

Executive Summary

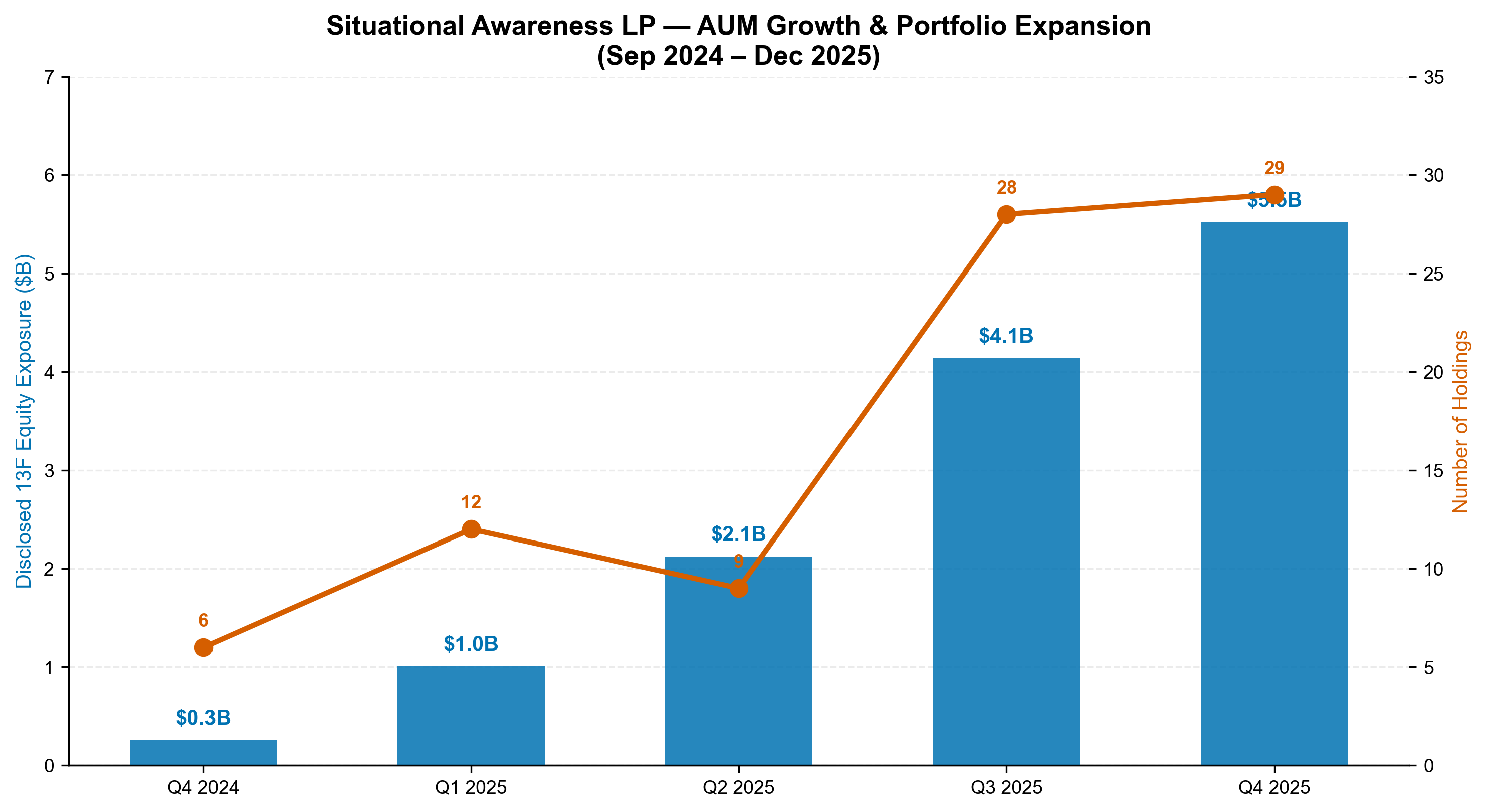

Leopold Aschenbrenner — a 24-year-old former OpenAI researcher — has built one of the most remarkable first-year hedge funds in modern financial history. Situational Awareness LP grew from $225 million in disclosed U.S. equity exposure at launch (September 2024) to $5.52 billion across 29 holdings by Q4 2025, with total discretionary regulatory AUM of approximately $9.3 billion. The fund beat the S&P 500 by 47% in its first six months and generated over 96 percentage points of alpha through early 2026.

His thesis is deceptively simple: AGI arrives by ~2027, and the most undervalued assets in financial markets are the physical infrastructure bottlenecks — power, compute, memory, optics — that constrain the buildout. He buys the bottlenecks, shorts what AI displaces, and rotates aggressively as the constraint migrates through the technology stack.

This report examines the intellectual foundation, the 13F portfolio evolution, the investment playbook, how his predictions have held up, and the risks that could break the thesis.

1. The Man Behind the Thesis

Biography

- Born ~2001 in Germany to two medical doctors

- Enrolled at Columbia University at 15; graduated at 19 (2021) as valedictorian with dual degrees in economics and mathematics-statistics

- Won a grant from Tyler Cowen’s Emergent Ventures (2021)

- Co-authored Existential Risk and Growth with Philip Trammell at Oxford’s Global Priorities Institute

- Interned at FTX Future Fund (2022) — resigned before the collapse

- Joined OpenAI’s Superalignment team (2023)

- Fired from OpenAI (April 2024) after submitting an internal memo criticising the company’s security posture and warning about Chinese espionage

- Published “Situational Awareness: The Decade Ahead” (June 2024) — a 165-page manifesto

- Launched Situational Awareness LP (September 2024)

- Has invested almost all of his personal net worth in the fund

Key Backers

Anchor capital from:

- Patrick and John Collison (Stripe co-founders)

- Nat Friedman (Meta AI product lead, former GitHub CEO)

- Daniel Gross (co-lead Meta Compute)

The fund counts “West Coast founders, family offices, institutions, and endowments” among investors.

“Aschenbrenner pitched the fund by rejecting a venture-capital structure: AGI was going to be so consequential to the global economy that the only way to fully capitalise on it was to express investment ideas in the most liquid markets in the world.”

2. The Intellectual Foundation

2.1 The Academic Paper: Existential Risk and Growth

Co-authored with Philip Trammell at Stanford’s Digital Economy Lab. Core finding:

The risk-minimising rate of technological growth is typically positive and often high.

This is the philosophical licence for the entire fund: accelerating AI development (and investing in its infrastructure) reduces existential risk rather than increasing it. Every position the fund has ever taken traces back to this academic result.

2.2 The Manifesto: Situational Awareness: The Decade Ahead

Published June 2024. 165 pages. Five chapters (full PDF):

| Chapter | Core Claim |

|---|---|

| I. From GPT-4 to AGI: Counting the OOMs | AGI by 2027 is “strikingly plausible” — extrapolating compute (~0.5 OOM/yr), algorithmic efficiency (~0.5 OOM/yr), and “unhobbling” |

| II. From AGI to Superintelligence | Intelligence explosion follows within 1-3 years; AI systems automate AI research itself |

| III. Racing to the Trillion-Dollar Cluster | Industrial mobilisation on the scale of wartime production is required; power grids must expand by tens of percent |

| IV. Lock Down the Labs / Superalignment | Current AI safety and security are fundamentally inadequate |

| V. The Free World Must Prevail | US-China AI race is the defining geopolitical contest of the century |

The “Counting the OOMs” Framework:

Aschenbrenner quantifies AI progress along three compounding vectors:

1. Compute — GPU training clusters doubling every ~1 year (~0.5 orders of magnitude/year)

2. Algorithmic efficiency — Better architectures and training methods (~0.5 OOM/year)

3. “Unhobbling” — Removing constraints on models (from chatbot → agent → autonomous researcher)

“GPT-2 to GPT-4 took us from ~preschooler to ~smart high-schooler abilities in 4 years. Tracing trendlines… we should expect another preschooler-to-high-schooler-sized qualitative jump by 2027.”

2.3 The One-Sentence Investment Thesis

AGI is a 2027 event; superintelligence is a 2028–2030 event; the markets have not priced in either the exponential trendlines or the industrial mobilisation they require. Therefore: buy the bottlenecks of the buildout (power, compute, memory, optics, fabs) and short what AI eats.

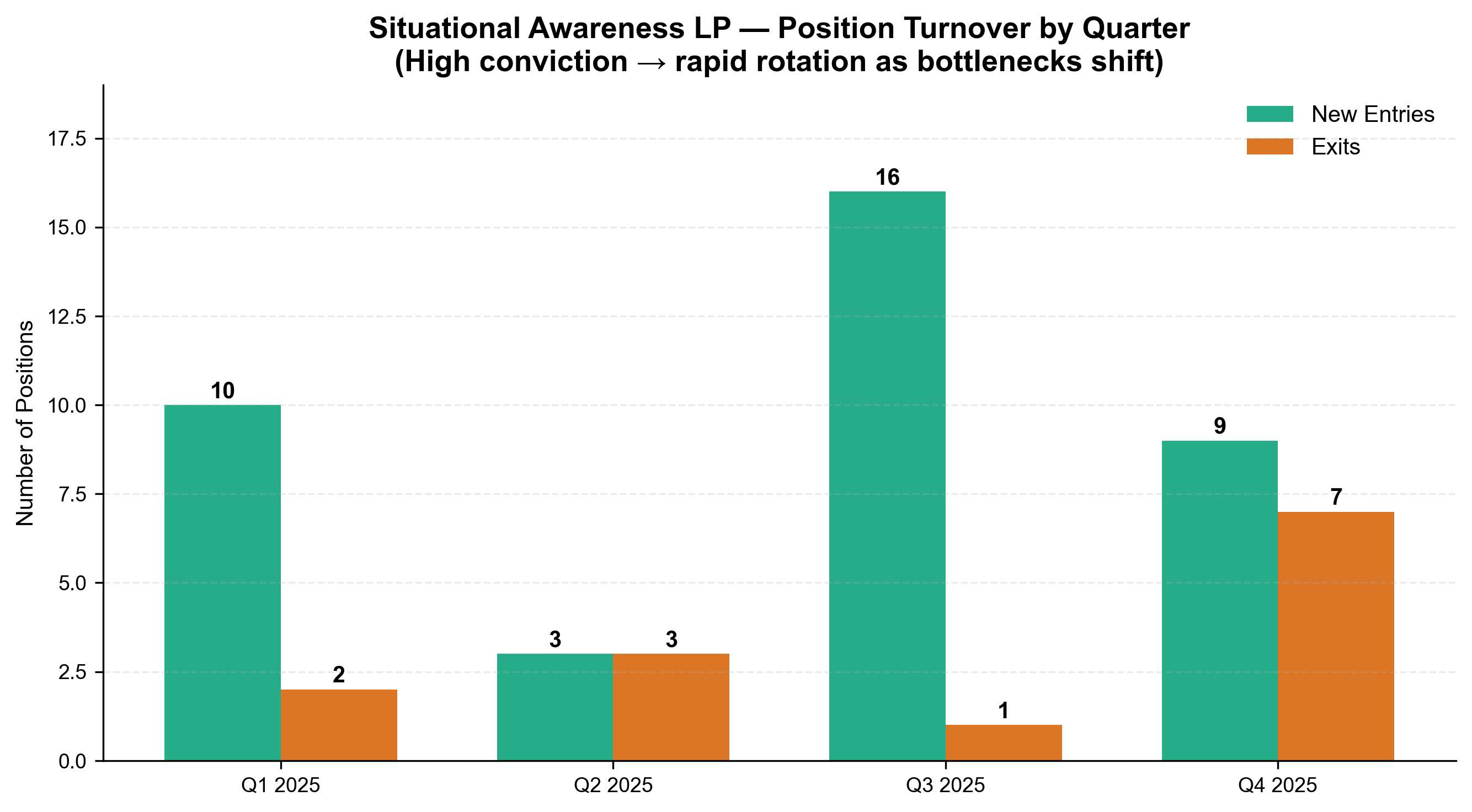

3. The 13F Portfolio — Quarter-by-Quarter Evolution

Source: SEC EDGAR via OpenBB SDK. CIK: 0002045724. All values in $M. 13F reflects long equity + call options only — no shorts, bonds, FX, or macro positions. Filed with 45-day lag.

Q4 2024 — $254.8M (6 holdings) — Phase 1: Semiconductors & Power IPPs

| # | Company | Value ($M) | Weight | Sector |

|---|---|---|---|---|

| 1 | Marvell Technology | $86.8 | 34.1% | Semiconductors |

| 2 | Vistra Corp | $59.1 | 23.2% | Power/Energy |

| 3 | Vertiv Holdings | $51.7 | 20.3% | Data Centre Cooling |

| 4 | Talen Energy | $28.0 | 11.0% | Power/Energy |

| 5 | Constellation Energy | $21.6 | 8.5% | Nuclear/Power |

| 6 | Modine Manufacturing | $7.7 | 3.0% | Thermal Management |

Thesis expression: Classic semiconductor picks (Marvell) + power producers that would benefit from data centre electricity demand (Vistra, Talen, Constellation). The “GPU era” bet.

Q1 2025 — $1.0B (12 holdings) — Phase 2: The Intel Conviction

| # | Company | Value ($M) | Weight |

|---|---|---|---|

| 1 | Intel Corp | $459.6 | 45.7% |

| 2 | Broadcom | $117.2 | 11.7% |

| 3 | Onto Innovation | $71.2 | 7.1% |

| 4 | Vistra Corp | $61.8 | 6.1% |

| 5 | Modine Manufacturing | $55.0 | 5.5% |

| 6 | EQT Corp | $52.9 | 5.3% |

| 7 | CoreWeave | $45.4 | 4.5% |

Key moves: Exited Marvell and Vertiv. Put 46% of the portfolio into Intel — a massively contrarian bet on a chipmaker Wall Street had written off. Added CoreWeave (GPU cloud) and Core Scientific (first crypto miner position). This was the DeepSeek moment (January 2025): when everyone panicked about Chinese AI, Aschenbrenner bought.

Q2 2025 — $2.1B (9 holdings) — Phase 3: The Semi ETF Hedge

| # | Company | Value ($M) | Weight |

|---|---|---|---|

| 1 | VanEck Semiconductor ETF | $570.1 | 26.9% |

| 2 | Intel Corp | $453.3 | 21.4% |

| 3 | Broadcom | $328.5 | 15.5% |

| 4 | Vistra Corp | $247.0 | 11.6% |

| 5 | Core Scientific | $136.5 | 6.4% |

Key insight: The VanEck Semi ETF position likely represents a short hedge against the broader semiconductor sector, while remaining long specific names (Intel, Broadcom). This is the first clear evidence of the long/short structure described in fund marketing.

Q3 2025 — $4.1B (28 holdings) — Phase 4: The Bitcoin Miner Pivot

Massive expansion. Added 16 new positions in a single quarter:

| New Positions | Category |

|---|---|

| Nvidia ($298M), TSMC ($75M), Broadcom ($76M) | Semiconductors |

| Bloom Energy ($44M) | Off-grid power |

| Cipher Mining, Riot Platforms, HUT 8, Bitdeer | Bitcoin miners → AI data centres |

| Lumentum ($68M), Coherent ($17M) | Optical interconnects |

| Micron ($50M), SanDisk ($13M), Western Digital ($18M) | Memory/Storage |

| Galaxy Digital ($93M) | Crypto/digital infrastructure |

Thesis shift: Bitcoin miners are the play — they already have the land, the power contracts, and the cooling infrastructure. They’re pivoting from mining BTC to hosting AI workloads. This is the “cheap compute + cheap electrons” trade.

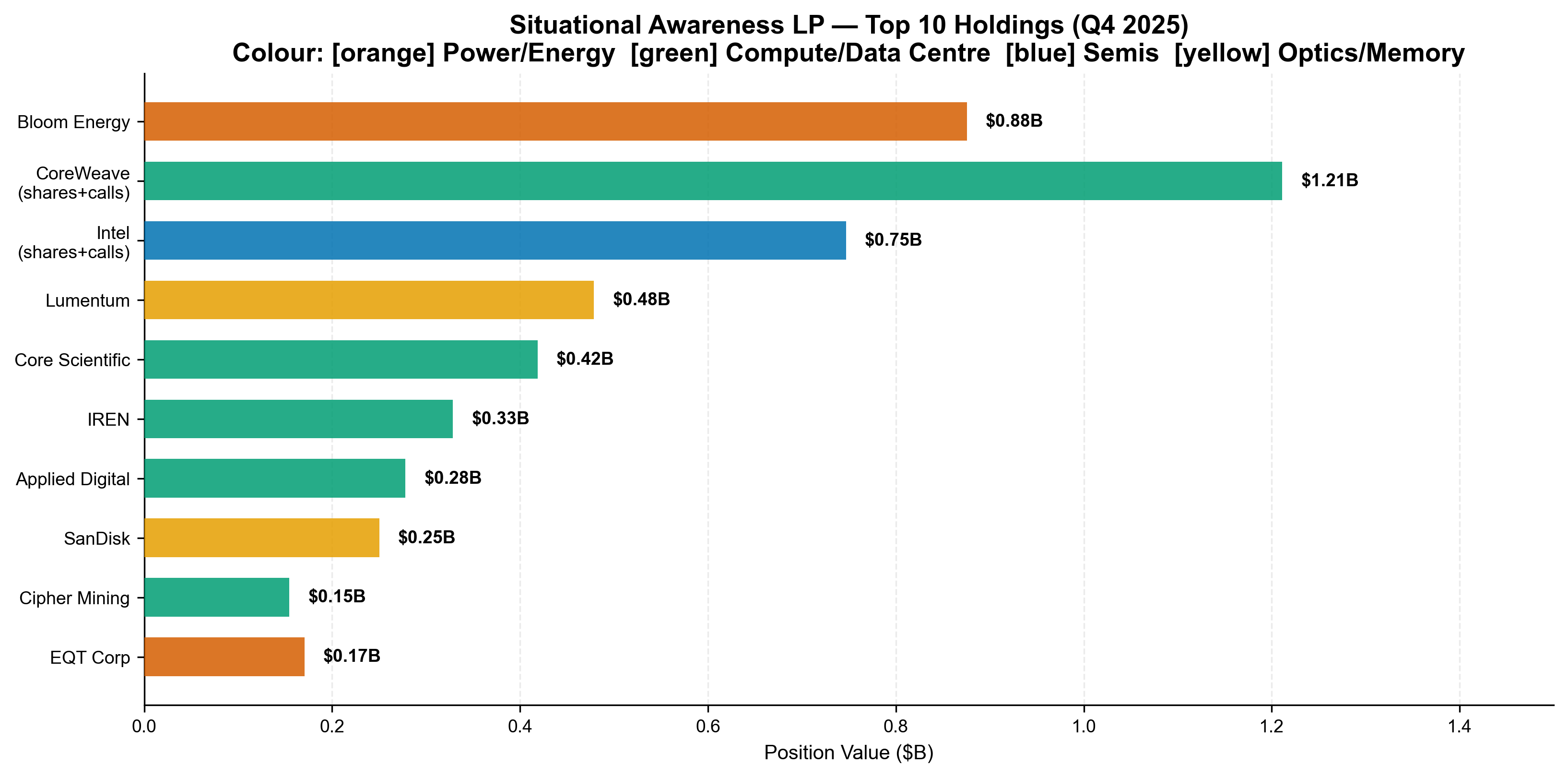

Q4 2025 — $5.5B (29 holdings) — Phase 5: Off-Grid Power & Optics

| # | Company | Value ($M) | Weight | Category |

|---|---|---|---|---|

| 1 | Bloom Energy | $875.5 | 15.9% | Off-grid fuel cells |

| 2 | CoreWeave (shares+calls) | $1,211.2 | 22.0% | GPU cloud |

| 3 | Intel Corp | $746.8 | 13.5% | Semiconductors |

| 4 | Lumentum | $478.6 | 8.7% | Optical interconnects |

| 5 | Core Scientific | $418.7 | 7.6% | Crypto → AI data centre |

| 6 | IREN | $328.6 | 6.0% | Crypto → AI data centre |

| 7 | Applied Digital | $278.0 | 5.0% | AI data centre |

| 8 | SanDisk | $250.2 | 4.5% | Memory/storage |

Major exits: Nvidia, TSMC, Vistra, Broadcom, VanEck Semi ETF. Exited the “consensus” AI trade entirely.

New entries: Kilroy Realty (data centre real estate), Infosys (as a short/put — betting AI coding tools displace IT outsourcing), WhiteFiber, Power Solutions International, Babcock & Wilcox, Liberty Energy, CleanSpark, Bitfarms.

The Bloom Energy thesis: The power grid simply cannot keep pace with AI data centre demand. Bloom Energy’s solid oxide fuel cells deliver reliable, on-site, off-grid power — bypassing grid constraints entirely. Oracle has validated this with 2.8 GW of fuel cell orders. The $875M position had already appreciated to ~$2.2B by May 2026 (a ~176% return).

“Most of Wall Street piled into model developers and chipmakers. Aschenbrenner focused on megawatts instead. So far, that call is paying off in spectacular fashion.”

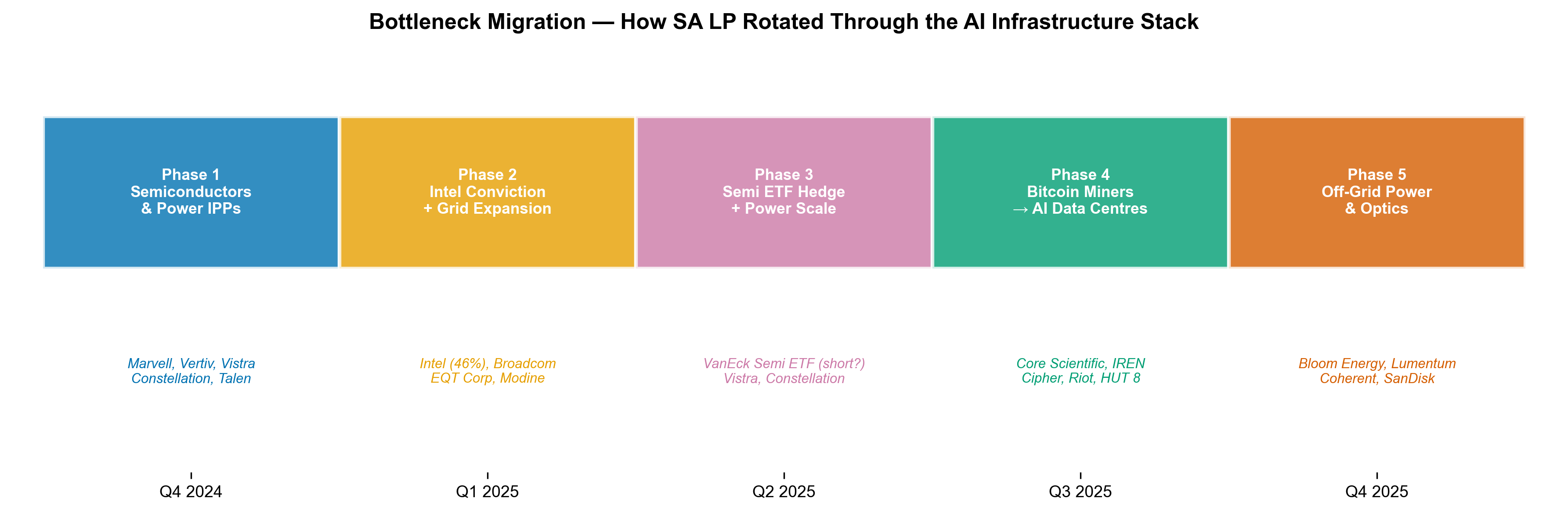

4. The Bottleneck Migration Framework

The portfolio’s most distinctive feature is not what it holds, but how it rotates. Aschenbrenner follows the bottleneck as it migrates through the AI infrastructure stack:

| Phase | Quarter | Bottleneck | Key Holdings |

|---|---|---|---|

| 1 | Q4 2024 | GPUs & power demand | Marvell, Vertiv, Vistra |

| 2 | Q1 2025 | Chipmaking capacity (contrarian Intel bet) | Intel (46%), Broadcom, EQT |

| 3 | Q2 2025 | Power grid expansion | Vistra, Constellation, VanEck Semi hedge |

| 4 | Q3 2025 | Compute hosting (crypto miners → AI) | Core Scientific, IREN, Cipher, Riot |

| 5 | Q4 2025 | Off-grid electricity + optical interconnects | Bloom Energy, Lumentum, Coherent |

The migration logic:

1. First, GPUs were scarce → buy semi companies

2. Then GPUs became abundant, but the grid couldn’t power them → buy power producers

3. Then power producers were priced in, but no one had the data centres to house the GPUs → buy Bitcoin miners pivoting to AI hosting

4. Then data centre capacity was growing, but the grid still couldn’t keep up → buy off-grid power (fuel cells)

5. Throughout, the data needed to move faster between GPUs → buy optical interconnect companies

5. Investment Playbook — The Seven Rules

Distilled from the thesis, the filings, and available transcripts:

Rule 1: Buy the Constraint, Not the Headline

Never owned Nvidia, Microsoft, Amazon, Google, or Meta. His largest position was a fuel cell company. The bottleneck is where the alpha lives.

Rule 2: Follow the Bottleneck as It Migrates

The constraint shifts over time (GPUs → power → data centres → off-grid power → optics). Rotate aggressively when the market catches up.

Rule 3: Exit When Priced In

Sold Nvidia, TSMC, Vistra, Broadcom, and Constellation Energy as they became consensus plays. By Q4 2025, exited the entire “obvious” AI trade.

Rule 4: Concentrate with Conviction

Just 6 holdings at launch. Single positions at 46% of portfolio (Intel). Diversification is not a feature — conviction is.

Rule 5: Use Options to Layer Conviction

Heavy call option positions on Intel, CoreWeave, and Bloom Energy. These aren’t hedges — they’re leveraged expressions of thesis confidence.

Rule 6: Go Activist When the Market Is Wrong

Filed a 13D on Core Scientific (17.7M shares, 5.8% stake) — signalling intent to push the company’s pivot from crypto mining to AI infrastructure hosting.

Rule 7: Buy the Panic

During the DeepSeek panic (January 2025), when markets sold off on fears of Chinese AI catching up, Aschenbrenner bought aggressively. Contrarian timing is a feature.

6. Fund Performance & Scale

| Metric | Value | Source |

|---|---|---|

| Launch date | September 2024 | Fortune |

| Initial disclosed equity | ~$225M (Q4 2024 13F) | SEC EDGAR |

| Q4 2025 disclosed equity | $5.52B | SEC EDGAR |

| Total regulatory AUM | ~$9.3B (Dec 2025) | WhaleWisdom |

| First 6-month return | Beat S&P 500 by 47 percentage points | Capitalists Substack |

| Total return (early 2026) | >100% YTD | Latticework/MOI Global |

| Alpha over S&P 500 | 96+ percentage points | MOI Global |

| Number of holdings | 6 → 29 (Q4 2024 → Q4 2025) | SEC EDGAR |

| Bloom Energy return | ~176% (Q4 2025 → May 2026) | Motley Fool |

Caveat: 13F filings show only long positions. The fund’s true performance includes shorts, options, international holdings, and leverage that are not publicly disclosed. The ~14:1 implied leverage ratio means disclosed equity exposure significantly exceeds actual capital.

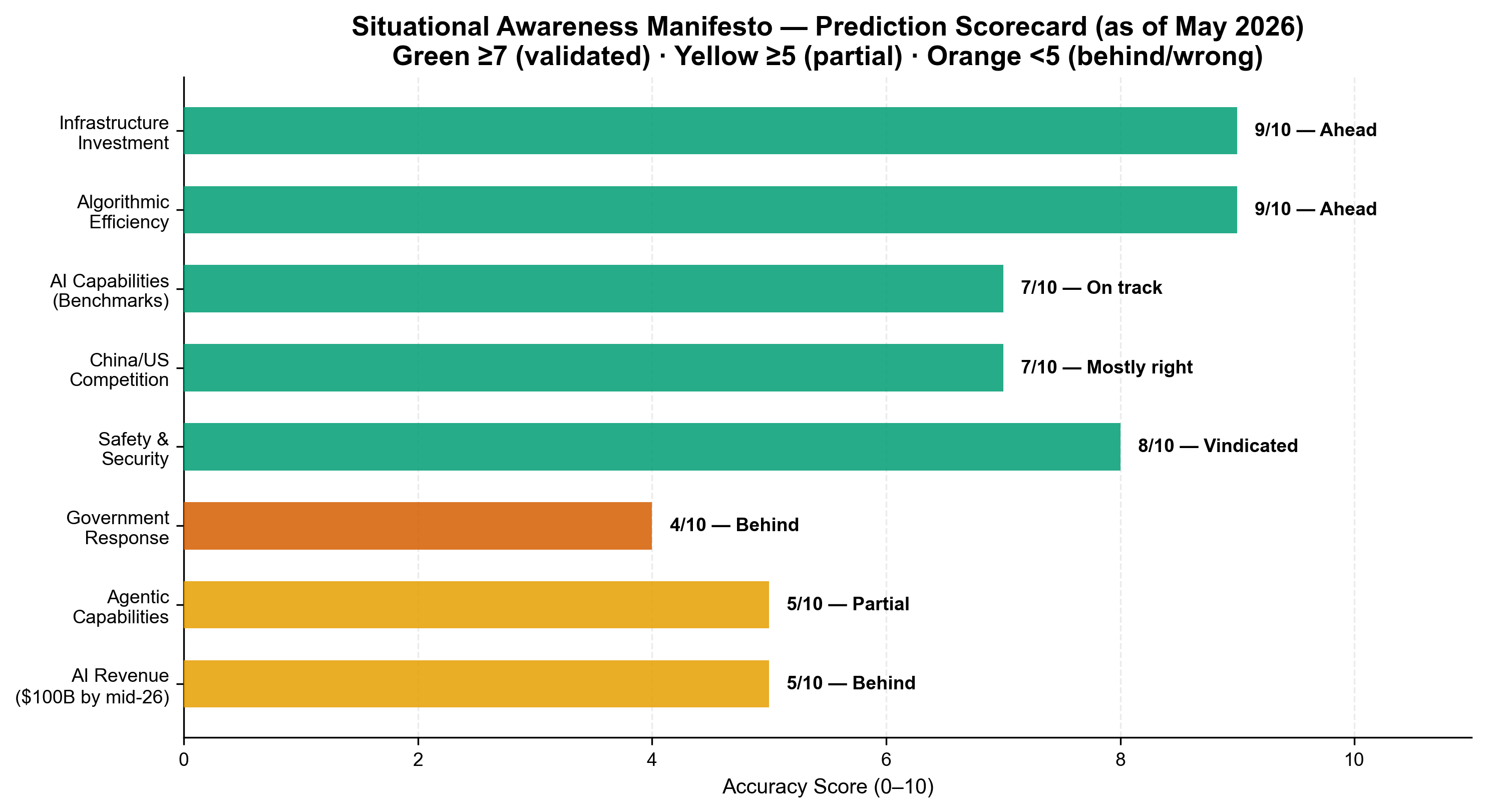

7. Prediction Scorecard — How Has the Manifesto Held Up?

The EA Forum conducted a systematic evaluation of the manifesto’s predictions as of March 2026:

What He Got Right (Score ≥7)

| Prediction | Status | Evidence |

|---|---|---|

| Infrastructure investment will explode | Ahead of schedule (9/10) | Trillion-dollar capex plans are real; every 6 months another zero added |

| Algorithmic efficiency will compound | Ahead (9/10) | DeepSeek’s innovations, test-time compute breakthroughs |

| AI capabilities on benchmarks | On track (7/10) | Benchmarks broadly saturated, though qualitative “shocking leap” hasn’t landed as dramatically described |

| China/US competition intensifies | Mostly right (7/10) | 7nm chips, espionage (Linwei Ding conviction), $2.5B chip smuggling, both sides opted out of responsible AI military declaration |

| Safety & security remain inadequate | Vindicated (8/10) | State-actor exploitation, race-dynamic pressure on safety, as predicted |

What He Got Wrong or Partially Wrong

| Prediction | Status | Evidence |

|---|---|---|

| Government response would mobilise | Behind (4/10) | No “Manhattan Project for AI” materialised; regulation slower than predicted |

| Agentic capabilities (drop-in coworker) | Partial (5/10) | Tool use advancing but “drop-in remote worker” not here yet; 2027 deadline hasn’t passed |

| AI revenue would hit $100B run rate by mid-2026 | Behind (5/10) | Best is ~$60B (OpenAI); market is behind his expectation |

| Open source would fade | Wrong | Capable open-source models thriving at the frontier (DeepSeek, Llama) — this is his most consequential error |

| China couldn’t innovate independently | Partially wrong | DeepSeek introduced genuine architectural innovations (Multi-head Latent Attention, fine-grained MoE) — not just distillation |

The Unresolved Question: AGI by 2027

“The AGI-by-2027 timeline is unresolved. It looked implausible six months ago, but recent capability jumps (particularly on software engineering tasks) have made it more credible again.”

Polymarket currently prices the probability of OpenAI announcing AGI before 2027 at ~13%.

8. Criticism & Risk Register

8.1 Intellectual Criticism

Timeline skepticism:

“Aschenbrenner’s argument relies on the leap of faith that researchers can overcome these problems through scaling alone… He never proves why this will happen, even in the face of counterevidence.”

— Lawfare

Sloppy reasoning allegations:

“Leopold Aschenbrenner’s weird conversion of human brainpower into LLM tokens/minute and his completely unrigorous claims about unhobbling are quintessential examples of how so much of the discourse about near-term AGI is based on hazy, sloppy reasoning.”

— EA Forum: “Questionable Narratives of Situational Awareness”

Counterargument — it doesn’t matter if he’s right about AGI:

The investment thesis works even if AGI doesn’t arrive by 2027. Power demand from AI data centres is real regardless. The infrastructure buildout is happening. The bottleneck migration is observable. The positions profit from the buildout, not from AGI itself materialising.

8.2 Financial Risks

| Risk | Severity | Detail |

|---|---|---|

| Concentration | High | Single positions at 15-46% of portfolio; top 5 holdings = ~60%+ |

| Implied leverage | High | ~14:1 leverage ratio; massive call option positions amplify returns and losses |

| AGI timeline dependency | Medium | If the buildout slows or AI winter occurs, every position suffers simultaneously |

| 13F opacity | Medium | Only shows longs; shorts, derivatives, and international holdings are invisible |

| Bottleneck migration speed | Medium | If the constraint shifts faster than he repositions, he’s holding yesterday’s trade |

| Regulatory/political | Medium | Data centre moratoriums, energy policy changes, crypto regulation shifts |

| Single-factor thesis | Medium | Entire portfolio is a correlated bet on one macro trend; no diversification by design |

8.3 The Bubble Question

“As AI bubble warnings mount, a 23-year-old’s $1.5 billion hedge fund shows how prophecy turns into profits”

The fund’s growth from $225M to $5.5B in 12 months is partly returns and partly new capital inflows. Separating the two is impossible from public filings alone. The 22x growth in disclosed equity exposure vs. ~100% reported returns suggests significant new capital is flowing in, amplifying the growth narrative.

9. Key Takeaways

-

The thesis is fundamentally about physics, not AI. Aschenbrenner’s edge isn’t predicting when AGI arrives — it’s understanding that electricity, cooling, and data interconnects are the binding constraints regardless of timeline.

-

Bottleneck migration is the alpha generator. The portfolio’s rapid rotation (38 new entries, 13 exits across 4 quarters) reflects a dynamic model of where value is accumulating — not a static bet.

-

The “buy the panic” philosophy works until it doesn’t. Buying during the DeepSeek crash was genius in retrospect. But a fund with 14:1 implied leverage and 46% in a single stock is one bad quarter away from catastrophic drawdown.

-

His most consequential error — underestimating open source — doesn’t hurt the fund. Open-source AI models thriving means more demand for infrastructure, not less. The thesis is robust to this prediction failure.

-

The fund is a single-factor trade. Every position is correlated to the same macro variable: AI infrastructure capex growth. This is both its strength (extreme focus) and its vulnerability (zero diversification).

-

The intellectual pedigree is genuine. Unlike most hedge fund stories, there is a traceable intellectual lineage from an academic growth-economics paper → a 165-page manifesto → a precisely sequenced portfolio. This is not pattern-matching or momentum-chasing.

Appendix: Complete 13F Holdings by Quarter

Q4 2024 — $254.8M (6 positions)

| Company | Value ($M) | Weight | |---------|-----------|--------| | Marvell Technology | $86.8 | 34.1% | | Vistra Corp | $59.1 | 23.2% | | Vertiv Holdings | $51.7 | 20.3% | | Talen Energy | $28.0 | 11.0% | | Constellation Energy | $21.6 | 8.5% | | Modine Manufacturing | $7.7 | 3.0% |Q1 2025 — $1,005.6M (12 positions)

| Company | Value ($M) | Weight | |---------|-----------|--------| | Intel Corp | $459.6 | 45.7% | | Broadcom | $117.2 | 11.7% | | Onto Innovation | $71.2 | 7.1% | | Vistra Corp | $61.8 | 6.1% | | Modine Manufacturing | $55.0 | 5.5% | | EQT Corp | $52.9 | 5.3% | | CoreWeave | $45.4 | 4.5% | | Constellation Energy | $37.0 | 3.7% | | Core Scientific | $32.7 | 3.3% | | Talen Energy | $29.6 | 2.9% | | Applied Digital | $22.7 | 2.3% | | IREN | $20.5 | 2.0% |Q2 2025 — $2,123.0M (9 positions)

| Company | Value ($M) | Weight | |---------|-----------|--------| | VanEck Semiconductor ETF | $570.1 | 26.9% | | Intel Corp | $453.3 | 21.4% | | Broadcom | $328.5 | 15.5% | | Vistra Corp | $247.0 | 11.6% | | Core Scientific | $136.5 | 6.4% | | EQT Corp | $125.1 | 5.9% | | Constellation Energy | $103.0 | 4.9% | | IREN | $93.3 | 4.4% | | Applied Digital | $66.4 | 3.1% |Q3 2025 — $4,138.4M (28 positions)

| Company | Value ($M) | Weight | |---------|-----------|--------| | Intel Corp | $679.0 | 16.4% | | CoreWeave (shares) | $563.2 | 13.6% | | Core Scientific | $362.0 | 8.7% | | IREN | $338.9 | 8.2% | | CoreWeave (calls) | $316.7 | 7.7% | | Nvidia | $298.5 | 7.2% | | Vistra Corp | $252.3 | 6.1% | | VanEck Semi ETF | $195.8 | 4.7% | | CoreWeave (additional) | $191.6 | 4.6% | | Applied Digital | $139.1 | 3.4% | | Galaxy Digital | $92.6 | 2.2% | | Broadcom | $75.9 | 1.8% | | TSMC | $75.4 | 1.8% | | Cipher Mining | $72.3 | 1.7% | | Riot Platforms | $68.4 | 1.7% | | Lumentum | $67.9 | 1.6% | | EQT Corp | $66.3 | 1.6% | | Micron | $50.2 | 1.2% | | Solaris Energy | $46.0 | 1.1% | | Bloom Energy (shares) | $43.9 | 1.1% | | Tower Semiconductor | $34.0 | 0.8% | | HUT 8 | $20.9 | 0.5% | | Western Digital | $18.3 | 0.4% | | Coherent | $16.6 | 0.4% | | Bitdeer | $15.9 | 0.4% | | SanDisk | $12.9 | 0.3% | | Bloom Energy (calls) | $12.3 | 0.3% | | Seagate | $11.5 | 0.3% |Q4 2025 — $5,516.8M (29 positions)

| Company | Value ($M) | Weight | |---------|-----------|--------| | Bloom Energy (shares) | $875.5 | 15.9% | | CoreWeave (shares) | $774.4 | 14.0% | | Intel Corp (shares) | $746.8 | 13.5% | | Lumentum | $478.6 | 8.7% | | CoreWeave (calls) | $436.7 | 7.9% | | Core Scientific | $418.7 | 7.6% | | IREN | $328.6 | 6.0% | | Applied Digital | $278.0 | 5.0% | | SanDisk | $250.2 | 4.5% | | Cipher Mining | $154.5 | 2.8% | | EQT Corp (shares) | $133.0 | 2.4% | | Coherent | $88.6 | 1.6% | | Solaris Energy | $85.8 | 1.6% | | Tower Semiconductor | $84.9 | 1.5% | | Riot Platforms | $78.1 | 1.4% | | Kilroy Realty | $49.6 | 0.9% | | HUT 8 | $39.5 | 0.7% | | EQT Corp (calls) | $37.5 | 0.7% | | Bloom Energy (calls) | $35.5 | 0.6% | | WhiteFiber | $27.8 | 0.5% | | Power Solutions Intl | $24.7 | 0.4% | | Bitdeer | $20.0 | 0.4% | | CleanSpark | $16.6 | 0.3% | | Bitfarms | $16.2 | 0.3% | | Liberty Energy | $10.5 | 0.2% | | Infosys (put/short) | $8.9 | 0.2% | | ProPetro | $8.7 | 0.2% | | Babcock & Wilcox | $8.6 | 0.2% | | Intel Corp (calls) | $0.0 | 0.0% |Report generated 2026-05-08. 13F data: SEC EDGAR via OpenBB SDK (obb.equity.ownership.form_13f, provider: sec). Charts: matplotlib with Okabe-Ito palette. All 13F values reflect reported market value at quarter-end. 13F filings do not include short positions, derivatives (except calls), international holdings, or leverage.