Canva: Revenue Channels, Path to Profitability, and Valuation Resilience

Date: 2026-05-08

Topic: Canva’s revenue evolution, profitability story, and why SaaS multiple compression hasn’t dented its $42B private valuation

Status: Complete

Core Conclusions

- Canva’s revenue grew ~900x in a decade — from $4.4M (2016) to $4B ARR (2025) — powered by a freemium flywheel that converts free design users into paying subscribers, then into enterprise contracts.

- “Profitable” has a nuanced meaning at Canva: cash-flow positive for 7+ years, but ASIC statutory filings show hundreds of millions in net losses driven by non-cash stock-based compensation. The first true statutory profit ($26M) came only in FY2025.

- SaaS multiple compression hit Canva in 2022 (valuation fell from $40B → $26B) but has since recovered to $42B, because Canva’s growth rate (35-48%) far outpaces typical SaaS comps, its B2B enterprise segment is growing at 100%, and AI has become a growth tailwind rather than a displacement threat.

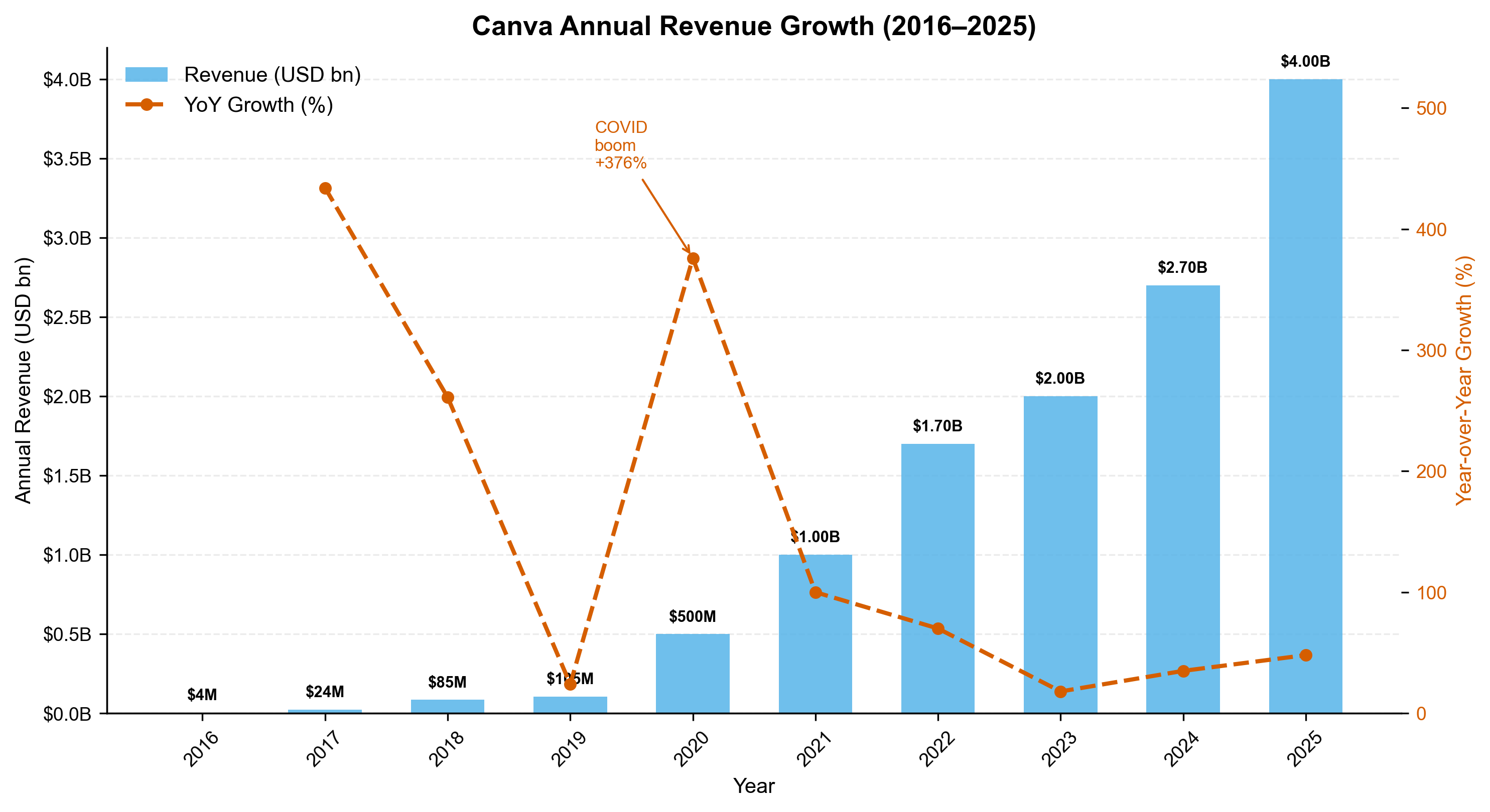

1. Revenue Growth Over Time

| Year | Revenue | YoY Growth |

|---|---|---|

| 2016 | $4.4M | — |

| 2017 | $23.5M | +434% |

| 2018 | $85M | +261% |

| 2019 | $105M | +24% |

| 2020 | $500M | +376% |

| 2021 | $1.0B | +100% |

| 2022 | $1.7B | +70% |

| 2023 | $2.0B | +18% |

| 2024 | $2.7B | +35% |

| 2025 | $4.0B ARR | +48% |

Sources: Electroiq Canva Statistics, Yahoo Finance / TechCrunch Feb 2026

Three distinct acceleration events drove this curve:

- 2017–2018: Product-market fit in the freemium/SMB segment. Canva’s visual simplicity displaced expensive desktop design tools for non-designers.

- 2020: COVID-19 pandemic caused an explosive +376% surge. Remote teams, educators, solopreneurs all pivoted to digital-first visual communication — Canva was the easiest on-ramp.

- 2024–2025 re-acceleration: Enterprise push + AI integration reversed the post-2021 growth slowdown. Cliff Obrecht (COO) credited the reacceleration mix as: 70% core flywheel optimisation, 10% international expansion, 20% AI integration.

“In the end, the thing that bails out our incompetence is your growth rate.”

— Cliff Obrecht, Canva COO (SaaStr, September 2025)

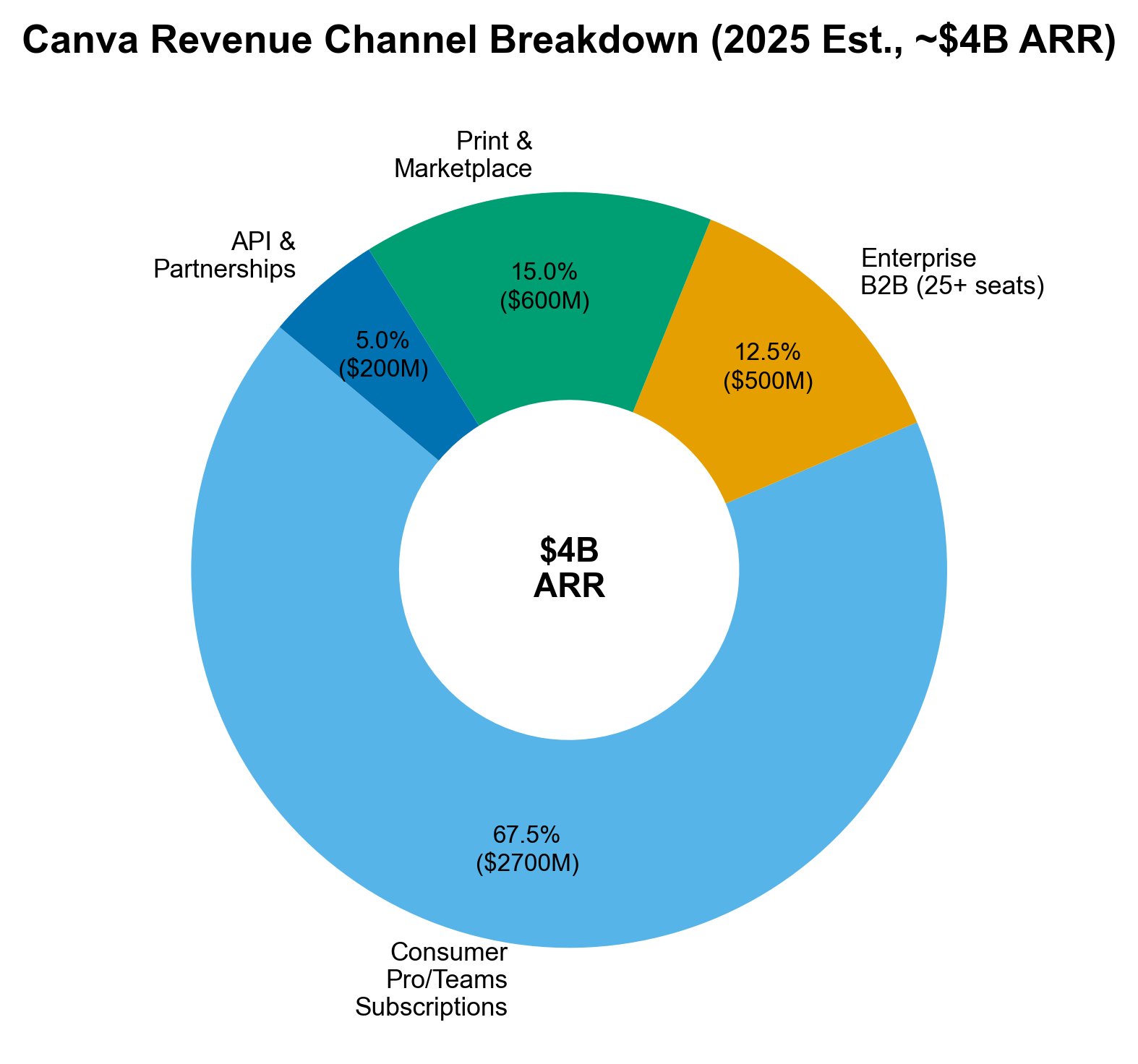

2. Revenue Channel Breakdown

Canva operates a multi-stream freemium SaaS model. The approximate 2025 breakdown:

2.1 Consumer / SMB Subscriptions (≈67% of revenue, ~$2.7B)

Canva’s core monetisation engine. Free users hit a “ceiling” on premium templates, brand assets, and AI tools, then upgrade to:

- Canva Pro: $12.99/month or $119.99/year per user. Unlocks 100M+ premium assets, background remover, Magic Resize, brand kits.

- Canva for Teams: $14.99/month for 5 users ($10/user/month), minimum 3 users. Adds real-time collaboration, shared brand folders, approval workflows.

As of end-2025, Canva had 31.2 million paid subscribers out of 265 million MAU — an ~11.8% paid conversion rate. A Canva Teams user paying $10/month yields ~$120 ARPU annually.

“The revenue breakdown follows this approximate distribution: subscription revenue from Canva Pro and Teams accounts for roughly 70-75% of total income.”

— Untaylored.com Business Model Analysis

2.2 Enterprise B2B (≈12.5% of revenue, ~$500M ARR, 100% YoY growth)

Canva Enterprise (25+ seats) launched as a fully-fledged product in May 2024. It includes SSO, advanced brand controls, centralised asset management, approval workflows, and enterprise-grade security.

Key data:

- $500M ARR by early 2026 (TechCrunch February 2026)

- 100% YoY growth — the fastest-growing segment

- Used by 95% of Fortune 500 companies

- Canva Teams average contract value increased 66% in 2025 (SaaStr)

Cameron Adams (co-founder, CPO) explained the strategic pivot:

“We had really strong grounding in small businesses and individuals, and enterprise wasn’t something we had focused on for a long time. We started looking more deeply into enterprise because we saw pockets of people using Canva within large organizations, and we needed to figure out how to unlock them properly.”

— Inc. Magazine, February 2026

2.3 Print & Marketplace (≈10-15% of revenue, ~$400-600M)

- Canva Print: physical printing of designs onto business cards, banners, T-shirts, invitations. Ships to 30+ countries. Pricing by product, volume, and country.

- Design Marketplace: Third-party creators sell premium templates and graphics. Canva takes 35% of the sale price; creators keep 65%. For Pro subscribers, royalty model is 50% of net Pro revenue.

- Design School: Free online courses (physical classes from $5), primarily a user acquisition/retention funnel rather than a major revenue line.

“Print services contribute approximately 15-20% through physical product fulfillment.”

— Untaylored.com

2.4 API & Partnerships (≈5%, ~$200M)

Enterprise API licensing, MCP server integrations (Canva is in top 10 referred domains from ChatGPT and Claude), and integration ecosystem fees. This segment is small today but growing rapidly as LLM referral traffic drives new user acquisition.

“By October 2025, users had more than 26 million conversations with the Canva app on ChatGPT.”

— TechCrunch February 2026

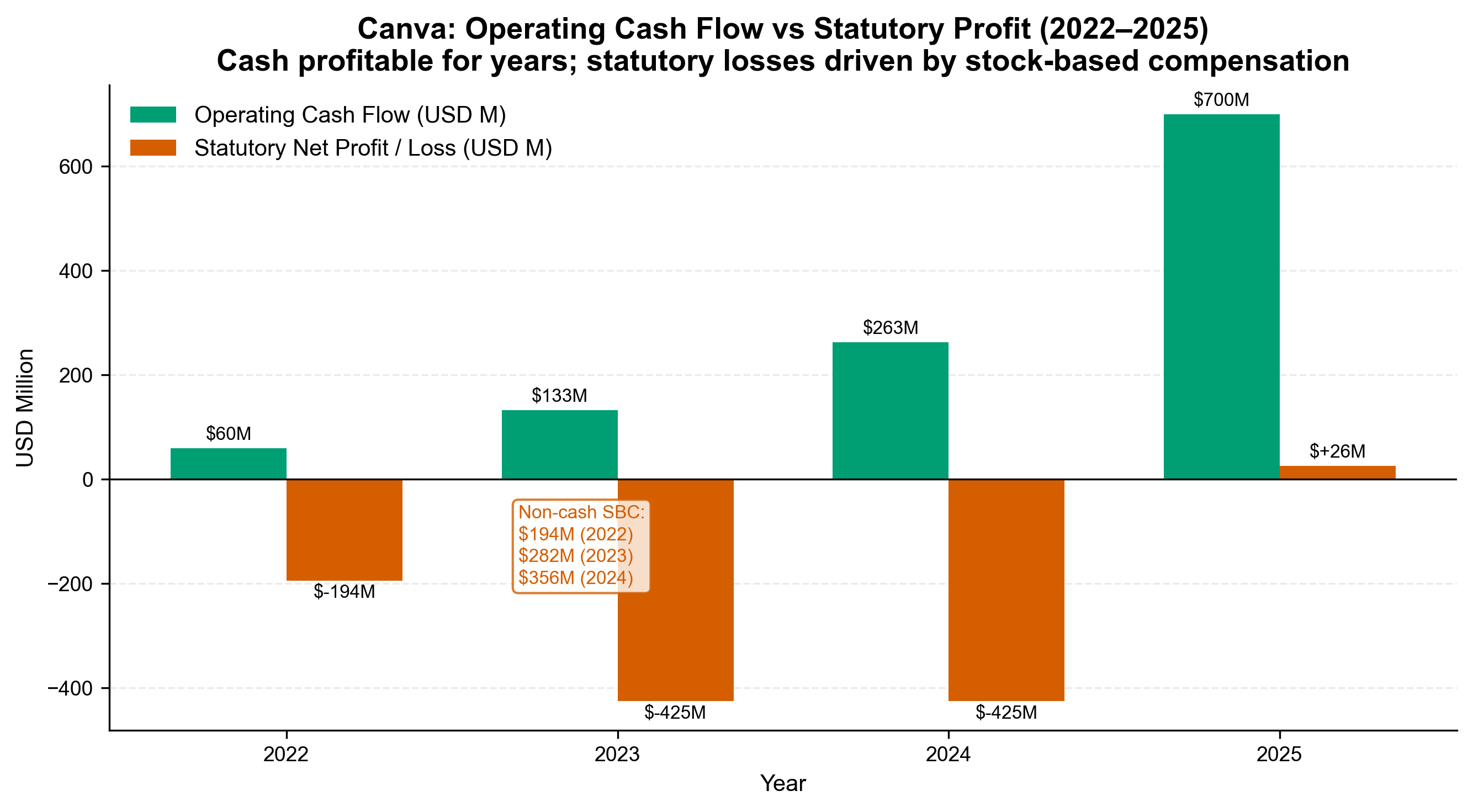

3. The Profitability Story — What “Profitable” Really Means

Canva claims to have been “profitable on an operating free cash flow basis for seven years in a row.” But its ASIC-filed accounts tell a different, nuanced story.

3.1 Operating Cash Flow: Genuine, Growing

| Year | Operating Cash Flow |

|---|---|

| 2022 | ~$60M (est.) |

| 2023 | $133M |

| 2024 | $263M |

This is real cash generated from operations — subscriptions collected exceed cash operating expenses. The FCF margin in 2024 was approximately 10-12% of revenue, with cash reserves of ~$699M (AUD ~$1B) by end-2024.

“Canva has been profitable on an operating free cash flow basis for several years.”

— Canva spokesperson, quoted in Startup Daily

3.2 Statutory Losses: The SBC Effect

ASIC filings for the Australian entity show:

| Year | Statutory Net Result | SBC (Non-cash) |

|---|---|---|

| 2022 | ~$(194M) loss | ~$194M |

| 2023 | $(425M) loss | $282M |

| 2024 | $(425M) loss | $356M |

| 2025 | $+26M profit | N/A |

The gap is almost entirely explained by stock-based compensation (SBC) — equity grants to employees recorded as expenses under accounting standards, but no cash leaves the business. This is standard practice for high-growth tech companies (Salesforce, Airbnb, and Stripe all show similar patterns).

The first statutory profit ($25.96M) came in FY2025, coinciding with 40% revenue growth at scale. The implication: Canva is now large enough that even after full accounting treatment of SBC, it earns a net profit.

“Canva’s Australian group booked a $25.96m profit after income tax on revenue of $3.02bn.”

— The Aussie Corporate, 2026

3.3 Why This Matters for Valuation

The distinction between cash profitability and statutory profitability directly shapes how investors assess Canva:

- Bears point to the $692M in cumulative losses (2022-2024) as evidence of unsustainable cost structure.

- Bulls note operating cash flow doubled in a year ($133M → $263M), the company has no debt, holds ~$1B cash, and hasn’t needed external funding since 2021.

- The first statutory profit in 2025 removes a key bear-case argument ahead of the expected IPO.

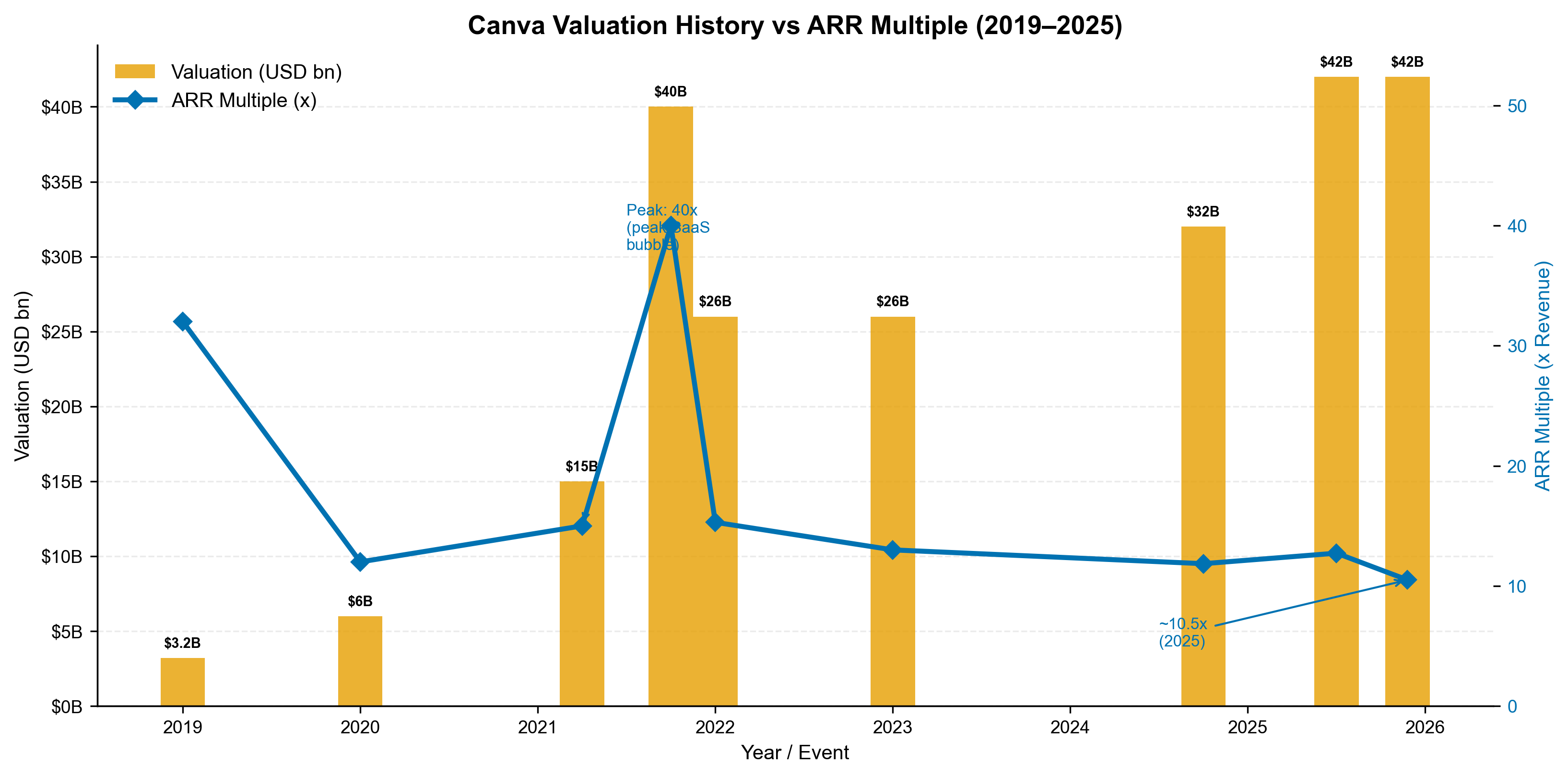

4. Why SaaS Multiple Compression Hasn’t Killed Canva’s Valuation

4.1 What Happened to SaaS Multiples

From 2021 to 2023, the SaaS sector went through a severe de-rating. Peak-2021 SaaS companies traded at 30-50x ARR; by 2023 that had compressed to 8-15x. Canva itself fell from $40B → $26B in 2022.

But unlike peers that stayed down, Canva’s private valuation recovered: $26B (2022-23) → $32B (Oct 2024) → $42B (Aug 2025).

4.2 The Key Reasons Canva Decoupled

① Growth rate is simply too high to be discounted like a median SaaS company

At 35-48% growth on $3-4B ARR, Canva is not a “value SaaS” story. Comparable public companies:

- Figma: ~40% growth, trades at ~11-12x ARR

- Adobe: ~10% growth, trades at 4.5-7x ARR

- Canva: ~35-48% growth at 4x Figma’s revenue → by comps, worth $44-72B

SaaStr’s Jason Lemkin:

“Canva at 35% is nearly on par with Figma at 40%. These are not meaningfully different growth rates at this scale — and Canva has 4x the ARR. Apply Figma’s current multiple to Canva’s $4B ARR and you get $44-48 billion.”

— SaaStr February 2026

② AI is a tailwind, not a threat

SaaS compression in 2024-2025 was partly driven by AI disruption fears — the thesis that LLMs would replace category-specific SaaS tools. For most design tools, this was a legitimate concern. For Canva, AI has accelerated growth:

- 800M monthly AI interactions (700% YoY growth in 2025)

- $370M acquisition of Leonardo.ai built a proprietary image/video generation backbone

- Canva is among the top 10 referred domains from ChatGPT — LLMs funnel users into Canva, not away from it

- Acquisition of Cavalry (motion graphics) and MangoAI (video generation) in 2026 to further embed AI

“We’re inverting that now. We’re becoming an AI platform with a bunch of design tools. So you can think of it more like a cursor for design.”

— Cliff Obrecht (TechCrunch February 2026)

③ B2B enterprise segment is re-rating the company upward

The $500M enterprise ARR (100% growth) is the key valuation driver for the IPO narrative. Enterprise SaaS commands higher multiples than consumer SaaS because:

- Higher average contract values ($50K-$500K+ vs $120/user/year)

- Lower churn (procurement friction vs subscription cancellation)

- Expansion revenue (seat-based growth within existing accounts)

- 95% Fortune 500 penetration means expansion is converting to new ARR at scale

The B2B segment alone growing at 100% — faster than Figma’s entire business — means investors can frame Canva as an enterprise platform story, not a design tool story.

④ Distribution moat is deepening, not commoditising

265 million MAUs is a distribution asset no competitor can replicate quickly. Canva’s SEO-first growth strategy (“understand search intent, deliver editable content”) is now being extended to LLM-first distribution via its MCP server and ChatGPT integration.

“We drove a lot of early days in Canva through Google, really understood people’s search intent, and delivered them content that they could then go into our product and edit. And so we really see ChatGPT or any of the LLMs as top-of-funnel acquisition platforms.”

— Cliff Obrecht (TechCrunch February 2026)

⑤ Balance sheet strength as a moat

Canva has not needed external funding since 2021 ($273M raised), yet holds ~$1B in cash. This is unusual for a pre-IPO company at this growth rate. It enables:

- Opportunistic acquisitions at compressed SaaS multiples (Affinity, Leonardo.ai, Cavalry, MangoAI)

- No dilution pressure on founders/employees

- IPO on their own terms, not out of necessity

“We’ve had a billion sitting on our balance sheet for ages — that’s a flex, people.”

— Cliff Obrecht (SaaStr September 2025)

4.3 The Remaining Bear Case

The bull case is well-constructed, but meaningful risks remain:

| Risk | Bear Argument |

|---|---|

| AI commoditisation | Gamma, Kittl, Adobe Express are unbundling Canva’s features at lower price points |

| Valuation framing | If IPO S-1 positions Canva as “design tool”, public market will apply Figma’s multiple (~10x) not a platform multiple (~20-40x), implying $40-48B — below or at par with last private round |

| SBC-adjusted losses | 2022-2024 accumulated $692M in statutory losses; institutional investors may penalise this |

| B2B durability | Enterprise at $500M ARR is only 12.5% of revenue; if growth slows from 100% to 30%, the re-rating thesis weakens |

| Microsoft/Google entrenchment | Both have design tools bundled into enterprise suites with virtually unlimited distribution |

A bear-case public market multiple of 6-8x ARR would yield $24-32B — below the last $42B secondary valuation. The difference is not about business fundamentals; it’s about which category frame analysts apply.

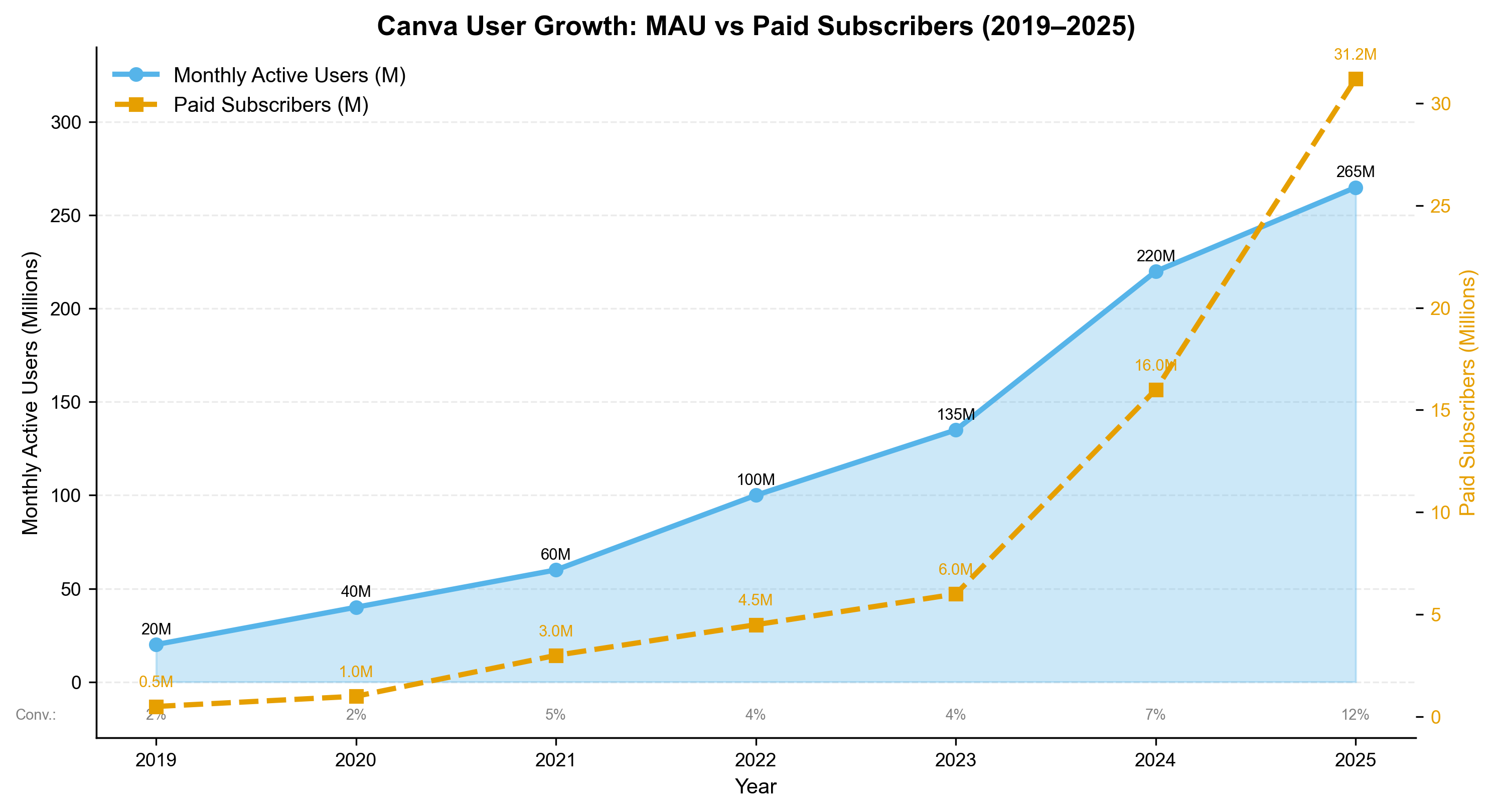

5. User Growth & Paid Conversion

| Year | MAU | Paid Subscribers | Conversion Rate |

|---|---|---|---|

| 2019 | 20M | 0.5M | 2.5% |

| 2020 | 40M | 1.0M | 2.5% |

| 2021 | 60M | 3.0M | 5.0% |

| 2022 | 100M | 4.5M | 4.5% |

| 2023 | 135M | 6.0M | 4.4% |

| 2024 | 220M | 16.0M | 7.3% |

| 2025 | 265M | 31.2M | 11.8% |

The paid conversion rate jumped sharply in 2024-2025 — from ~4.5% to 11.8% — likely driven by three factors:

1. Enterprise launch (high-value seat-based contracts replace individual conversions)

2. AI tool gating (premium AI features like Magic Design, Magic Write require Pro)

3. Geographic price localisation (lower-priced tiers in Pakistan, Uruguay, Morocco, Jamaica unlocked previously free markets)

The combination of more users and higher conversion is what makes Canva’s revenue re-acceleration so powerful. Revenue per user is also rising as enterprise contracts carry significantly higher ARPU than consumer Pro.

6. Cross-Validated Findings

| Claim | Sources Confirming |

|---|---|

| $4B ARR by end-2025 | TechCrunch (Feb 2026), SaaStr (Aug 2025), Inc. Magazine (Feb 2026) |

| 7+ years operating cash flow positive | SaaStr, Sacra, Canva spokesperson statements |

| First statutory profit in FY2025 ($26M) | The Aussie Corporate (2026) |

| B2B $500M ARR at 100% growth | TechCrunch, Inc., SaaStr |

| $42B last secondary valuation | TechCrunch, SaaStr, AFR |

| 95% Fortune 500 adoption | Canva 2025 Wrap, multiple sources |

| Top 10 LLM-referred domains | TechCrunch February 2026 |

Contested / Single-source:

- Pre-2020 revenue figures vary between sources (2019: $105M vs $291M). The $105M figure is supported by the 376% growth narrative widely cited, and is adopted here.

- Operating cash flow for 2022 (~$60M) is an estimate; exact figure not publicly filed.

- 2025 operating cash flow (~$700M) is estimated from scaling trends; the ASIC FY2025 filing had not been fully parsed as of research date.

7. IPO Outlook & Valuation Scenarios

Canva has hired Zoom’s former IPO CFO Kelly and is preparing for a public listing “within a couple of years” per Cliff Obrecht. The IPO will likely occur in 2026-2027.

| Scenario | Multiple | Revenue Basis | Implied Valuation |

|---|---|---|---|

| Bear (design tool frame, Figma comps) | 10x | $4B ARR | $40B |

| Base (platform comps, growth premium) | 15x | $4B ARR | $60B |

| Bull (enterprise re-rating, AI premium) | 20x+ | $4-5B ARR | $80-100B+ |

The $42B secondary looks conservative under base-case assumptions. The real strategic question is whether Canva’s S-1 positions the company as a “design tool” (where Figma’s 10x multiple anchors expectations) or as a “visual communication platform for knowledge workers” (where ServiceNow’s 15-20x is the right comp).

“The category frame established in the S-1 will persist throughout the company’s public life.”

— Paul Syng Blog, February 2026

Sources

| Source | URL |

|---|---|

| TechCrunch: Canva $4B ARR, Feb 2026 | https://techcrunch.com/2026/02/18/canva-gets-to-4b-in-revenue-as-llm-referral-traffic-rises/ |

| Inc. Magazine: Cameron Adams Interview | https://inc-1-smart-business-story.beehiiv.com/p/canva-co-founder-cameron-adams-on-hitting-4-billion-arr-the-power-of-free-and-that-ipo-825a |

| SaaStr: Canva $4B ARR Valuation Analysis | https://www.saastr.com/canva-crosses-a-stunning-4b-arr-but-what-would-it-be-worth-today/ |

| SaaStr: Cliff Obrecht B2B Lessons | https://www.saastr.com/saas-at-scale-hard-won-lessons-from-cliff-obrecht-on-building-canva-from-0-to-4b-arr/ |

| The Aussie Corporate: ASIC Filings | https://theaussiecorporate.com/blogs/pickandscrollnews/canva-s-rapid-growth-masks-billion-dollar-losses |

| The Aussie Corporate: First Statutory Profit | https://theaussiecorporate.com/blogs/pickandscrollnews/canva-posts-first-statutory-profit-after-late-filings |

| Startup Daily: Cash Flow vs Losses | https://www.startupdaily.net/topic/business/profitiness-why-canvas-profitable-right-up-until-it-has-to-file-accounts-with-the-government/ |

| Electroiq: Canva Statistics | https://electroiq.com/stats/canva-statistics/ |

| Sacra: Canva Deep Dive | https://sacra.com/c/canva/ |

| Untaylored: Revenue Streams | https://www.untaylored.com/post/how-canva-makes-money-business-model-explained |

| Paul Syng: IPO Framing Risk | https://paulsyng.com/blog/the-figma-trap-why-canvas-ipo-language-is-costing-billions-before-they-even-file/ |

| Chayut Orapinpatipat: AI Disruption Analysis | https://chayuto.com/blog/ais-impact-on-saas-competition |

| AFR: Figma Warning for Canva | https://www.afr.com/technology/figma-plunge-sounds-warning-to-canva-investors-20250902-p5mrup |

| Canva 2025 Wrap | https://www.canva.com/newsroom/news/canva-2025-wrap/ |

| The Meridiem: SaaS Compression & Acquisitions | https://www.themeridiem.com/enterprise/2026/02/24/canva-stacks-ai-through-dual-acquisition-as-saas-valuations-compress |