Australian Private Property Sales: Why Agents Dominate and No “Airbnb for Real Estate” Exists

Date: 2026-05-08

Topic: Private property transactions in Australia, seller-side agent dominance, FSBO platforms, structural barriers

Sources: ABC News, The Guardian, ACCC, IBISWorld, OpenAgent, InfoTrack, SMH, REA Group filings

Core Conclusions

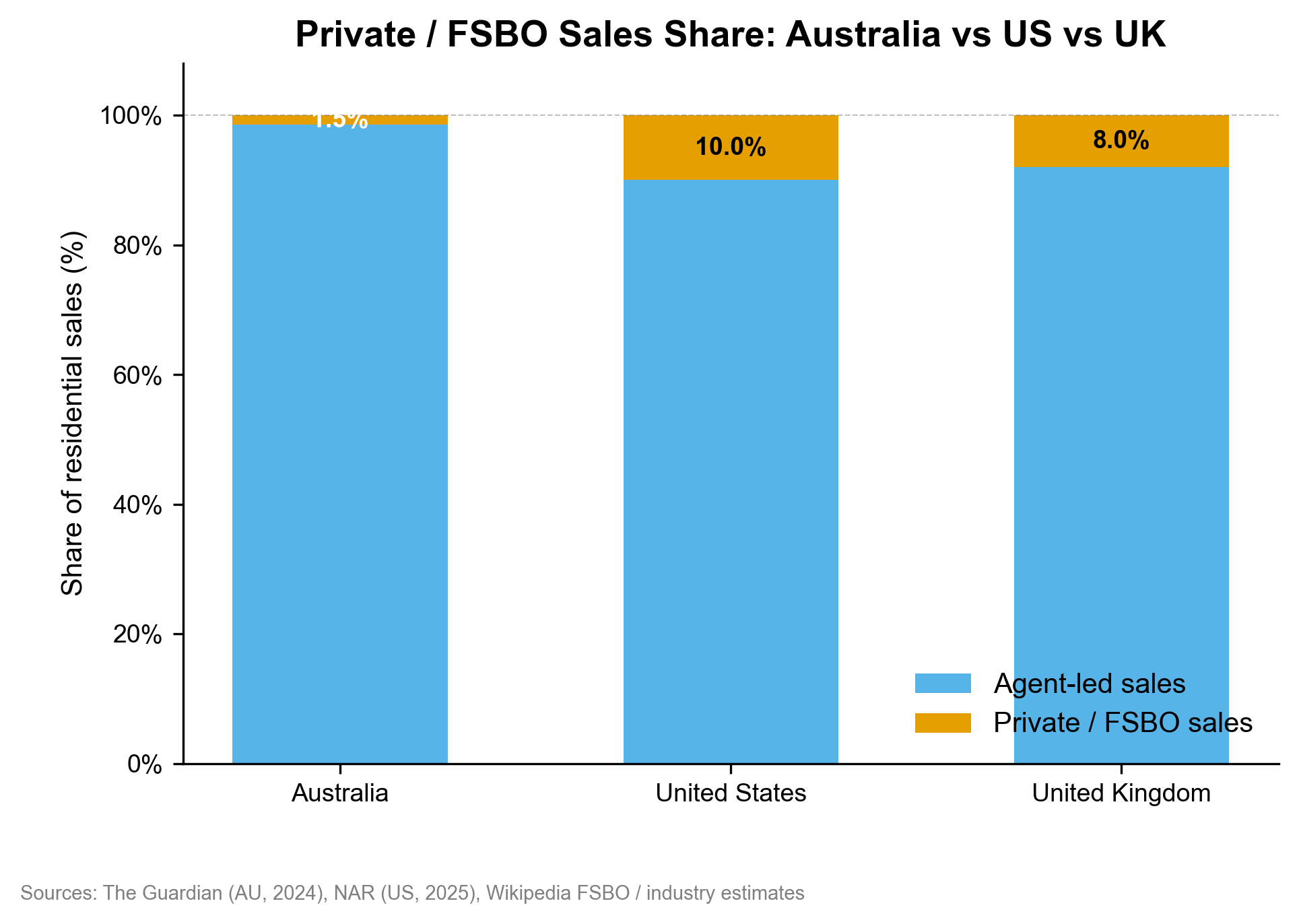

Australia is one of the most agent-dependent residential property markets in the world. Private (FSBO) sales account for only 1-2% of all residential transactions, compared to ~10% in the US and ~8% in the UK. The dominance of seller-side agents is not primarily a legal mandate — it’s structural. A layered set of moats keeps agents entrenched:

- A portal duopoly (realestate.com.au + Domain) that refuses direct access to private sellers

- An auction culture that legally requires licensed agents and auctioneers

- A licensing framework that makes listing on major portals impossible without a registered agency

- Commission economics that make agents the path of least resistance for most sellers

A handful of FSBO platforms exist and are growing, but they’ve remained a rounding error. There is no “Airbnb for real estate” in Australia, and the structural reasons are deep.

1. The Scale of Agent Dominance

The Australian real estate services industry generated $30.4 billion in revenue in FY2024-25, employing around 168,000 people across 46,520 businesses (IBISWorld 2025). Agent numbers grew 30% between 2014 and 2024.

InfoTrack’s 2025 State of Real Estate Report surveyed buyers and sellers directly: 91% of respondents engaged a real estate agent in their most recent transaction, up from 90% in 2024. This isn’t declining — it’s stable or rising slightly.

Private sales sit at an estimated 1-2% of the market (The Guardian, Sep 2024). By contrast, the US National Association of Realtors puts FSBO at around 10% of US home sales, and the UK has a comparable share through hybrid/online agents.

This gap isn’t accidental. It’s the product of deliberate structural design.

2. The Portal Duopoly: The Core Structural Barrier

The single most important reason private sellers struggle in Australia is portal access.

realestate.com.au and Domain.com.au collectively function as the mandatory distribution layer for residential property in Australia. Any property not on one of them effectively doesn’t exist to most buyers. REA Group’s realestate.com.au alone attracts over 12 million unique users monthly — at least 50% more views and listings than Domain (ACCC, via KOSEC, May 2025).

The critical fact: realestate.com.au does not allow private sellers to list directly. Only licensed real estate agencies can upload listings to the platform.

“Realestate.com.au restricts property listings to licensed real estate agents. This means private sellers cannot list their properties directly.”

This forces private sellers into one of two paths:

- Use a traditional agent (and pay commission)

- Use an FSBO intermediary platform that itself holds a real estate licence

FSBO intermediaries (Owner.com.au, ForSaleByOwner.com.au, PropertyNow, NoAgentProperty, MinusTheAgent, SaleByHomeOwner) solve this technically — they are licensed agencies that list on behalf of private sellers for a flat fee. But there’s a catch: REA charges private intermediaries double the listing rate.

Dimitri Chrisis, a Sydney vendor who ditched his agent mid-campaign, found this out directly:

“The cost to list his house on the site through a real estate agency was $3,200 for a premiere listing, but to sell privately using a private sales agent the cost was $6,200. ‘It is shocking — how can they be charging people [who want to buy a one-off premiere listing] double the price? It is very unfair.’”

REA Group’s Fee Trajectory

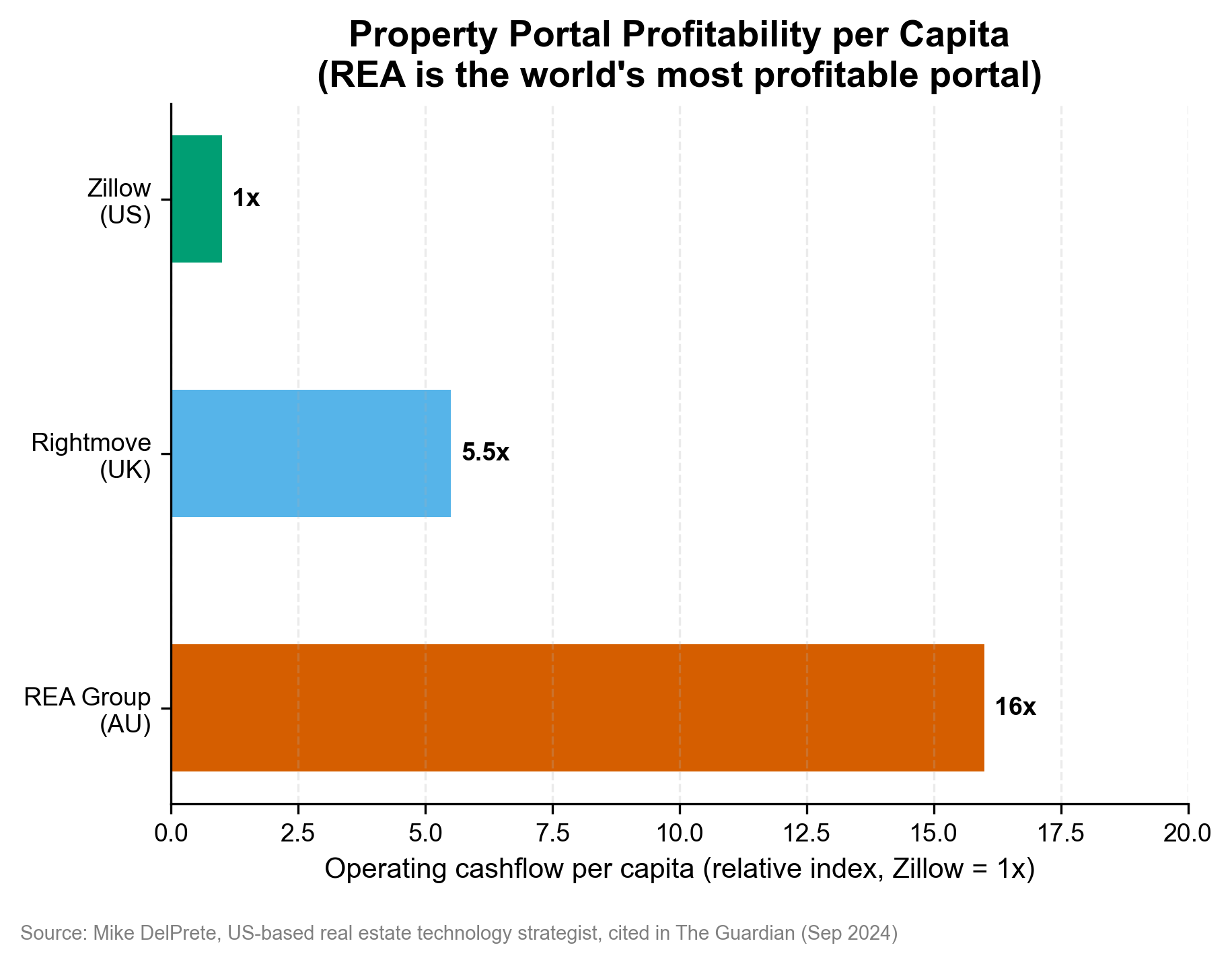

REA Group is majority owned by News Corp. It posted a net profit of $460.5 million in FY2024 on revenues of $1.5 billion — a 23% revenue increase year-on-year. Mike DelPrete, a US-based real estate technology strategist, called it bluntly:

“REA is the best in the world at this, REA is the most profitable real estate portal in the world… they are just printing money.”

REA’s operating cashflow per capita is 16 times that of Zillow and almost 3 times that of UK portal Rightmove. This is not a coincidence — it’s the result of a structural monopoly on the distribution layer.

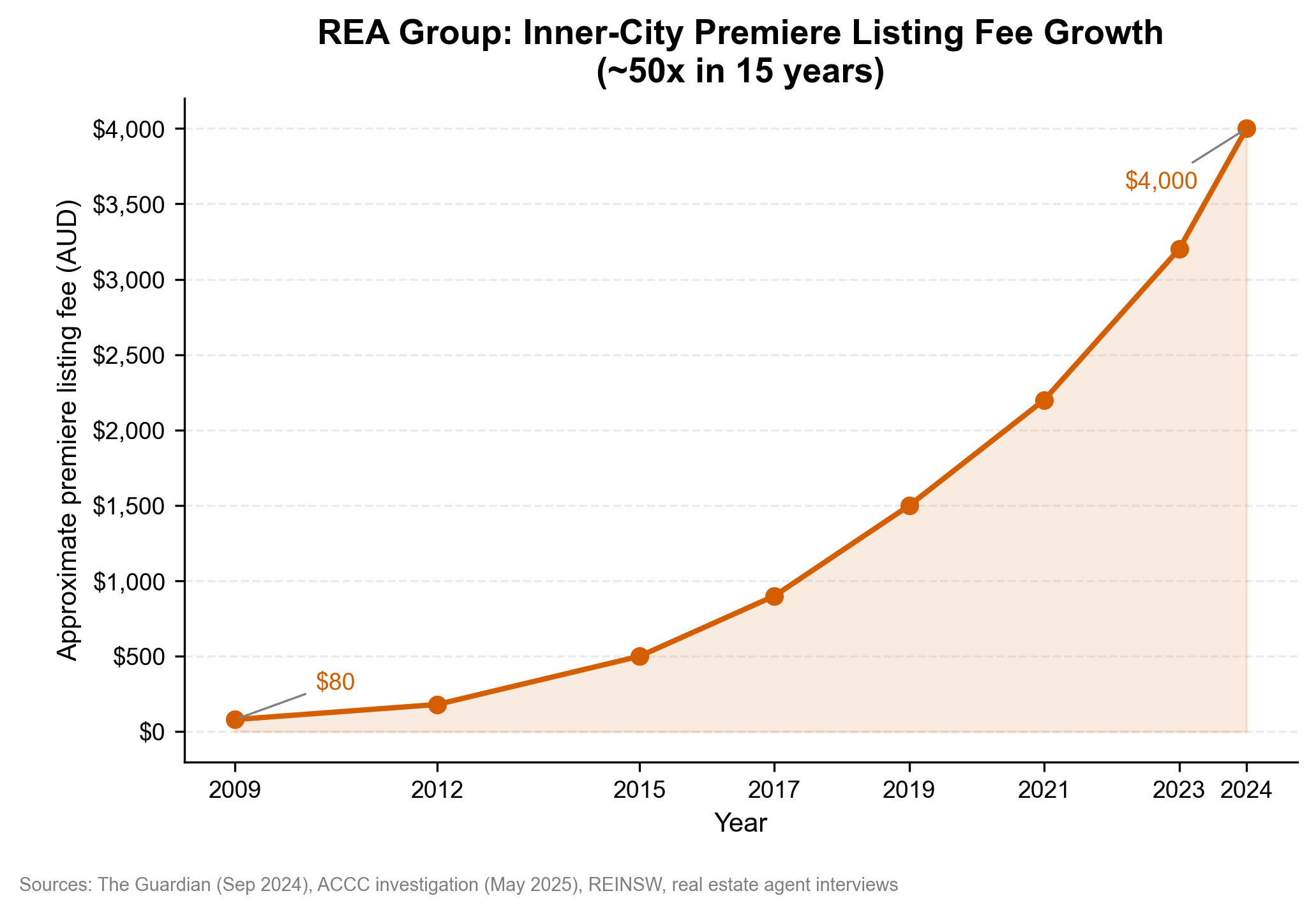

REA premium listing fees have increased ~5,000% (50x) in 15 years — from approximately $80 per top-tier listing in 2009 to $4,000 in inner-city Sydney and Melbourne in 2024.

The ACCC launched an investigation in May 2025. The Real Estate Institute of NSW’s CEO, Tim McKibbin, stated:

“These escalating costs significantly increase the burden for consumers and are clearly unsustainable.”

In Australia, sellers pay advertising costs directly — one of only ~3 markets globally where this is the case. In the US, agents upload to MLS databases (industry-owned, not-for-profit) at negligible cost. In the UK, agents bundle advertising costs into their commission. The Australian model puts REA Group at the apex of the transaction and extracts rent from every side.

3. The Auction Moat

Australia has an unusually strong auction culture — particularly in Melbourne and Sydney. This is one of the least-discussed but most powerful structural barriers to private sales.

Why Auctions Entrench Agents

Auctions in Australia are legally required to be conducted by a licensed auctioneer. You cannot hold an auction for your own property. An agent running an auction campaign has an almost unbreakable grip on the transaction — they prepare the Statement of Information, run open inspections over a 3-5 week campaign, call the auction, and negotiate on the day.

Industry insiders have anonymously confirmed what buyers advocates report publicly:

“Some sales agents have anonymously confirmed that auction processes are favourable for them, the sales agents. It may not usually favour the seller, but it usually benefits the sales agents.”

Agents prefer auctions because:

- They compress the campaign, reducing labour per transaction

- Unconditional contracts mean less post-auction negotiation

- They can run multiple auctions on the same day (efficiency)

- Higher clearance rates = marketing material for the agent

Data from REA shows auction sellers in Sydney earned significantly more than private treaty sellers in comparable suburbs — $19,100-$42,700 more on average depending on suburb (realestate.com.au). This makes the “use an agent for auction” pitch genuinely compelling, not just self-serving.

This is a key difference from Airbnb’s market. Short-term rentals didn’t require licensed operators. Residential property auctions in Australia do — by law.

4. Agent Commissions: The Cost and Why Sellers Still Pay

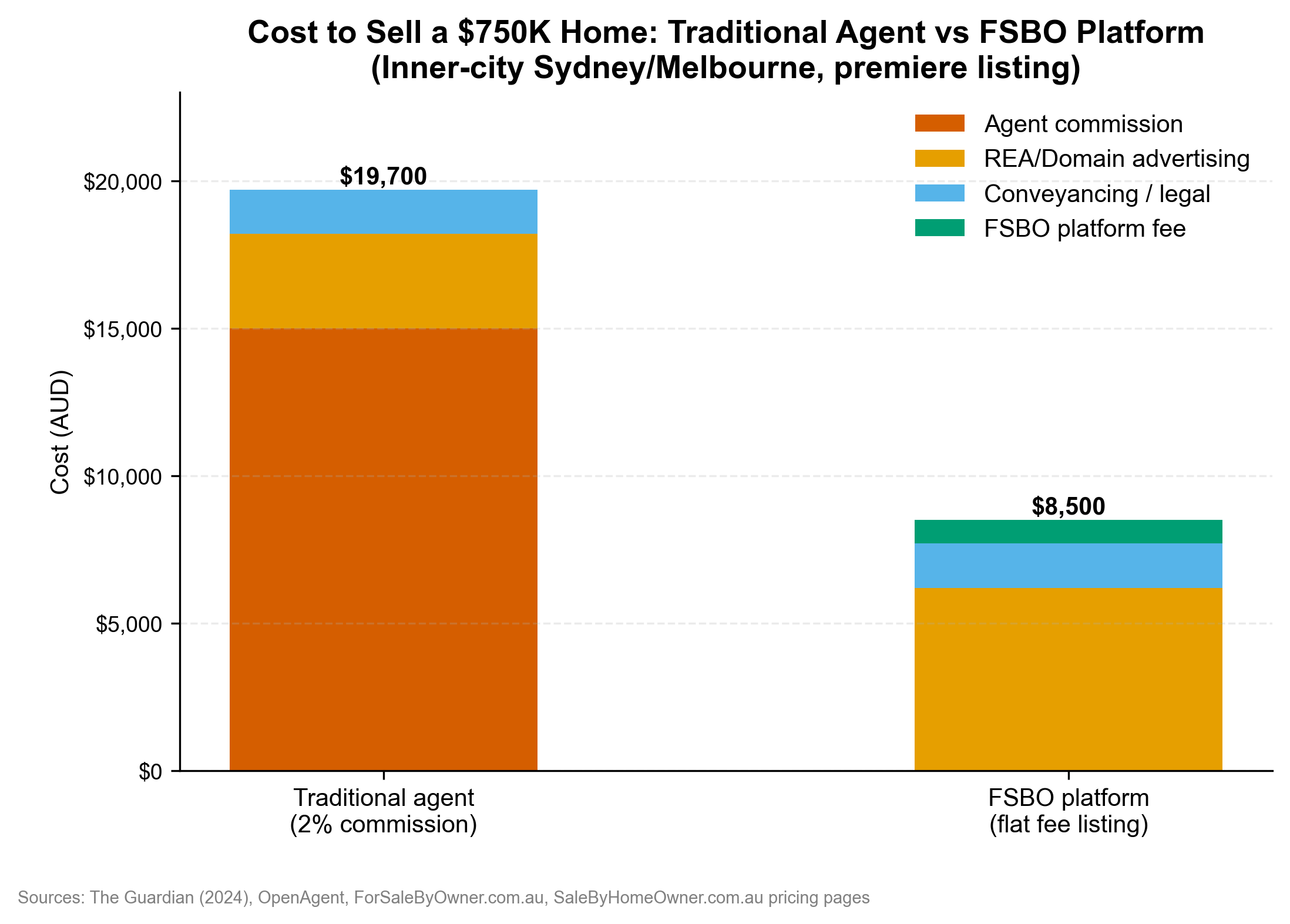

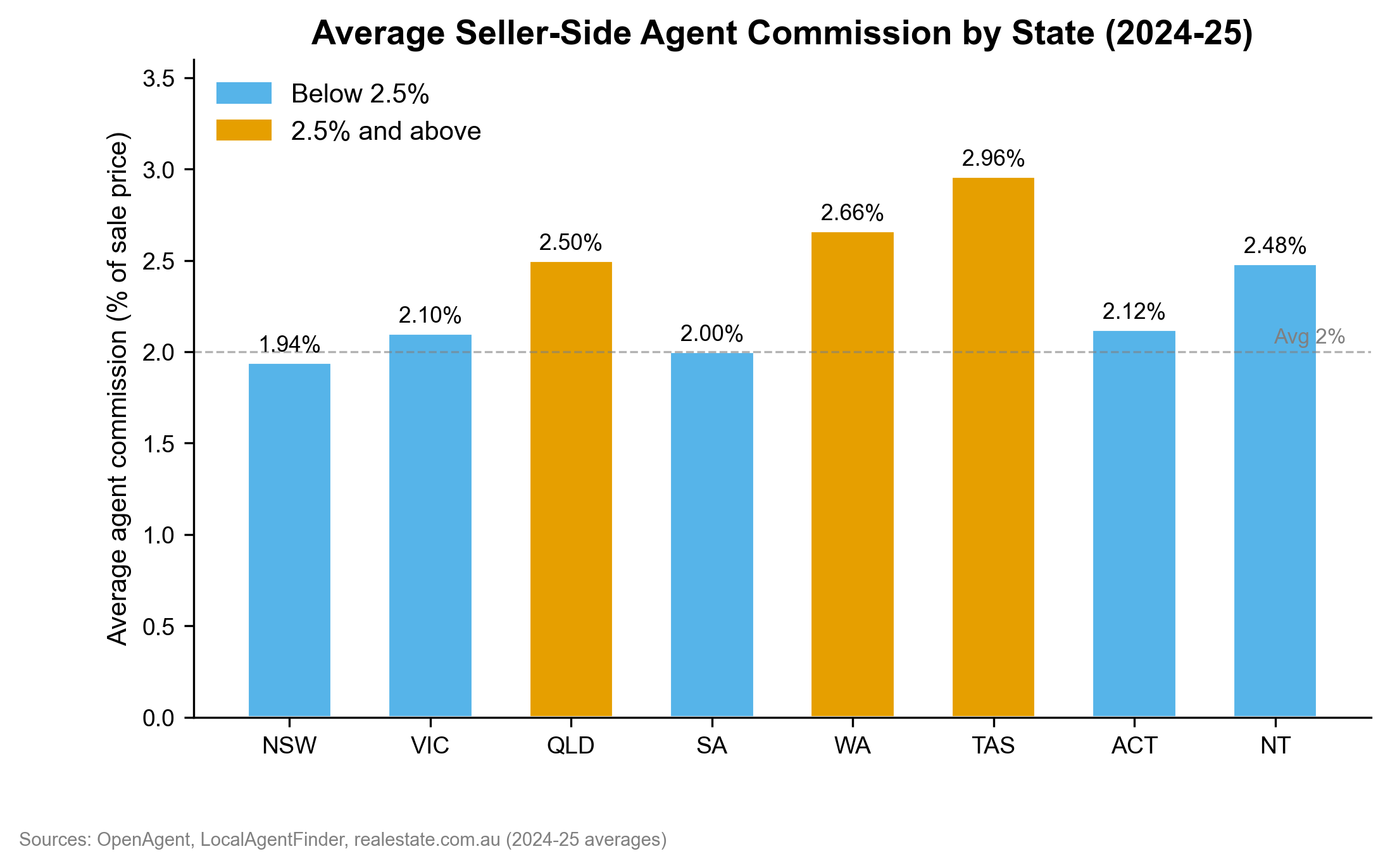

Average seller-side commissions range from 1.94% in NSW to 2.96% in Tasmania. The national average is approximately 2%.

On Australia’s median dwelling value of around $750,000, that’s roughly $15,000 in commission — plus separate advertising costs of up to $4,000 for a premiere REA listing. A typical agent-assisted sale in metropolitan Sydney or Melbourne costs a seller $18,000-$22,000 all up.

Why do sellers pay this willingly?

- Anchoring: sellers fear leaving money on the table. Agents are skilled at presenting their fee as recovered via higher sale prices

- Auction premium: data shows auctions genuinely do deliver higher prices in competitive suburbs

- Complexity shield: contracts of sale, vendor disclosure statements, cooling-off periods, settlement clauses — the legal complexity is real. Sellers want someone managing it

- Asymmetric information: agents know current comparable sales, buyer psychology, and negotiation tactics. First-time sellers don’t

- Social trust signal: a professional agent is a signal to buyers. A private seller can trigger suspicion (“what are they hiding?”)

As AHURI’s managing director Michael Fotheringham noted:

“Because of the way the market has become dependent on those [online real estate portals], these websites do signify a shift in the landscape.”

5. Existing FSBO Platforms: Who’s There and Why They Haven’t Scaled

Private sale platforms are not absent in Australia. They are small, growing, and structurally capped.

| Platform | Founded | Model |

|---|---|---|

| Owner.com.au | 1998 | Flat-fee listing portal, licensed agency |

| PropertyNow | 2006 | Agent-assisted private sales platform |

| ForSaleByOwner.com.au | ~2005 | Flat-fee, lists on REA/Domain |

| SaleByHomeOwner.com.au | — | Licensed agency, flat-fee intermediary |

| NoAgentProperty.com.au | — | DIY private sale with support |

| MinusTheAgent.com.au | — | Flat-fee multi-portal listing service |

These platforms saw 25-30% increases in inquiries in 2024 — driven by cost-of-living pressure pushing sellers to seek savings (ABC News, Sep 2024). ForSaleByOwner.com.au reported 30% growth; SaleByHomeOwner.com.au reported 25% growth. But the base is tiny.

Their structural ceiling is clear:

- They cannot access REA at agent rates — they pay the private seller surcharge, eroding the cost advantage

- They cannot run auctions (requires licensed auctioneer — they’d need to partner or hire one for every sale)

- REA’s terms of service effectively prevent them from building a competing consumer-facing portal using REA’s listing data

- They cannot build network effects at the property search layer — REA controls buyer attention, so sellers won’t migrate unless buyers do too

The Purplebricks Failure: A Case Study

Purplebricks launched in Australia in August 2016 with heavy TV advertising and a fixed-fee (£4,500) model. It exited in May 2019 after burning significant capital.

The core reasons:

“The problem was they picked up the UK Purplebricks model and plonked it here and it didn’t suit the Australian market. The managers assumed a lot of things that just weren’t workable. We have home auctions to start with, and the UK and USA don’t.”

— Adam Rigby, CEO of Upside Realty (SMH, May 2019)

The secondary killer was Purplebricks’ fee model — sellers paid whether or not the property sold. In a softening market (2017-2019), this was catastrophic for trust.

Evan Thornley, co-founder of LookSmart:

“Purplebricks was a ‘disruptor’ and they correctly belled the cat on the problem with the status quo. But their problem is they replaced it with something worse.”

6. Why This Can’t Be “Airbnb for Real Estate”

This is the structural heart of the question. Airbnb succeeded by:

1. Directly connecting hosts and guests on a two-sided marketplace

2. Owning the trust layer (reviews, insurance, identity verification)

3. Bypassing legacy incumbents who had no legal monopoly on short-term rentals

Australian residential real estate has none of these conditions:

| Condition | Short-term rental (Airbnb) | Australian residential property |

|---|---|---|

| Legal barrier to direct listing | None | Portals gate-keep to licensed agents |

| Incumbent controls distribution | No (hotels don’t own booking.com) | Yes — REA controls buyer attention |

| Trust / complexity risk | Moderate | Very high (contracts, stamp duty, settlement) |

| Transaction requiring licensed professional | No | Auctions require licensed auctioneer |

| Transaction frequency | High (users return often) | Very low (once per decade) |

| Geographic commodity | Yes (same cabin, same beach) | No (every property unique) |

The closest analogy isn’t Airbnb — it’s Uber trying to operate in a city where the taxi company owns the only working GPS network, charges private drivers 2x what it charges taxi companies to use it, and is legally required for any ride that starts with a public bid.

Why the US Has It Slightly Better

The US’s Multiple Listing Service (MLS) is the structural difference. The MLS is a network of ~580 regional, industry-owned databases. Agents upload listings at near-zero cost. Consumer portals (Zillow, Redfin) then aggregate MLS data under licence. The MLS is not-for-profit and agent-collective-owned. This creates two effects:

- Advertising costs to sellers are minimal

- FSBO sellers can often pay a flat fee to a broker to list on the local MLS and get consumer portal exposure

Australia has no MLS equivalent. REA and Domain are private, for-profit, and able to set pricing unilaterally.

7. What Would Have to Change

For a genuine private sale platform to achieve Airbnb-like scale in Australia, at least one of the following would need to happen:

Regulatory intervention on portal access. The ACCC investigation (2025) could lead to mandatory reasonable-access obligations for REA/Domain — forcing them to offer private sellers access at agent rates. This is the most plausible path. The ACCC’s Section 155 Notice to REA Group suggests the regulator is building a case.

Auction law reform. Allowing vendors to conduct their own auctions (or use a licensed auctioneer without an agent) would remove the most complete agent lock-in. No state government has proposed this.

A critical-mass buyer portal. If a property search portal achieved sufficient buyer audience without depending on REA’s data, private sellers could list there. Domain has tried and failed to close the gap. No new entrant has come close.

Cultural shift + cost-of-living pressure. The 25-30% increase in FSBO inquiries in 2024 shows cost pressure is nudging sellers. If median prices climb further and commission savings become undeniable (a $1.5m property saves $30,000), adoption could accelerate past the 2% floor.

Cross-Validation Notes

These findings are consistent across multiple independent sources:

- The 1-2% FSBO share was reported by The Guardian (Sep 2024), corroborated by the small absolute volumes reported by FSBO platforms

- REA’s portal dominance and fee levels confirmed by InfoTrack, ACCC investigation filings, REINSW, and Guardian reporting — all independently

- Purplebricks failure analysis consistent across SMH, The Negotiator (UK), SmartCompany, and Top Agents Playbook

- Auction preference by agents reported by industry insiders in multiple Australian markets, independently corroborated

Single-source data to note with caution:

- The 50x fee increase figure (“agents say”) — not independently audited, but directionally consistent with ACCC filings showing multi-hundred-percent increases

- State commission averages from OpenAgent and LocalAgentFinder — industry-adjacent sources with potential upward bias; treat as approximate

Key Takeaways

- Australia has one of the most entrenched agent-dominated property markets globally. Only 1-2% of sales are private, vs 10% in the US.

- The barrier isn’t legal — it’s structural. REA Group’s grip on the distribution layer, combined with state-by-state auction laws requiring licensed professionals, makes disintermediation nearly impossible.

- FSBO platforms exist and are growing, but are capped. They pay double listing fees, can’t run auctions, and can’t build buyer-side network effects.

- Purplebricks proved the market is hostile to foreign disruption models. The Australian auction culture is particularly difficult to work around.

- REA Group is under ACCC investigation (2025) for market dominance and pricing abuse. Regulatory action is the most likely catalyst for structural change.

- The “Airbnb for real estate” can’t exist in Australia until the portal access monopoly is broken or an MLS-like shared infrastructure is created — neither of which will happen without government or regulatory intervention.

Research conducted 2026-05-08. All URLs active at time of research.